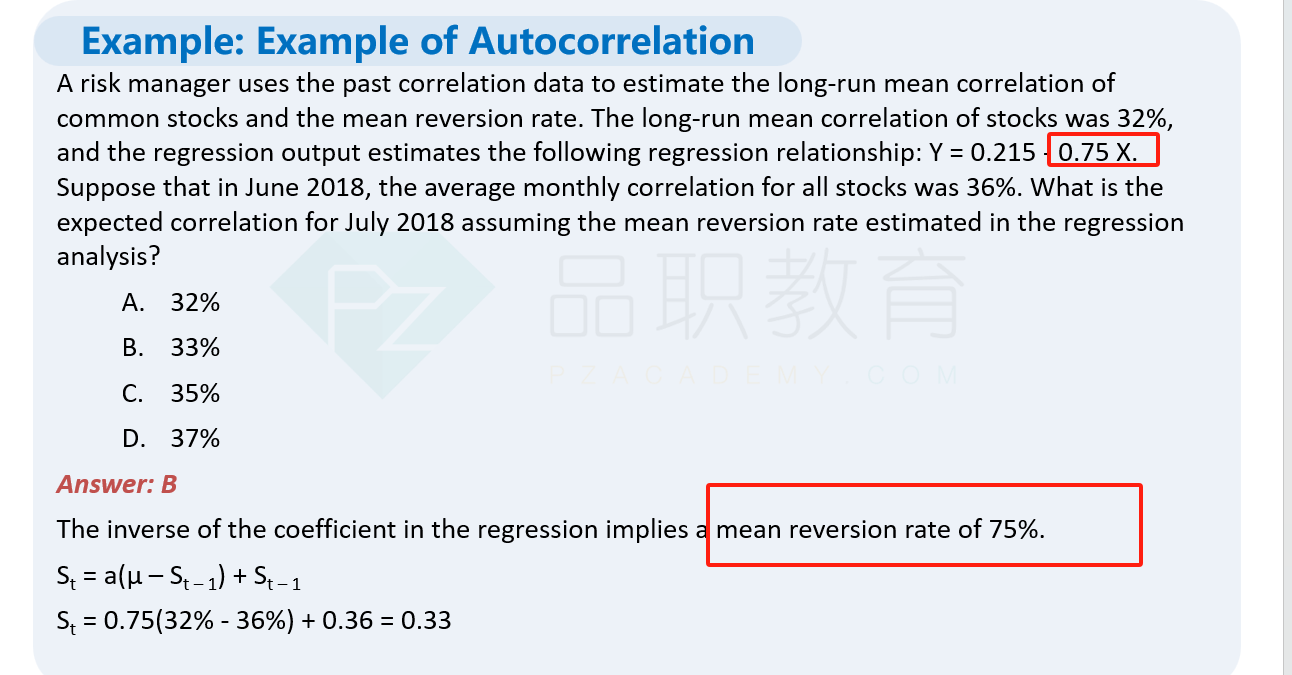

NO.PZ2023100703000064

问题如下:

Risk analyst uses data from the HS300 index over the past 260 weeks to estimate the long-term average correlation of the common stocks and mean reverting rate. And find the average long-term stock correlation of the HS 300 Index is 22%, and the regression output estimates the following regression relationship: Y = 0.34-0.55X. Assume that in first week of March 2020, the average weekly correlation of all HS300 stocks was 65%. Based on the mean reverting rate in regression analysis, what is the estimated one-week autocorrelation?选项:

A.0.219 B.0.23 C.0.35 D.0.45解释:

To find the estimated one-week autocorrelation based on the mean reverting process, we can use the following formula:

单期自相关率+均值回归率=1,所以自相关率只要拿1减去均值回归率,即1-0.55=0.45

老师好,我还是没太懂,题都没看明白,那两个ρ是指什么,跟题目没关系吗?说的是什么意思呢?如果我们把数据套用St=au+(1-a)st-1,能把题目的数据落到公式上吗?谢谢