NO.PZ2024030503000135

问题如下:

Question Under US GAAP, which of the following is a required financial statement disclosure concerning inventory?选项:

A.Only the material amount of income resulting from the liquidation of LIFO inventory B.Only the amount of any reversal of any write-down that is recognized as a reduction in cost of goods sold in the period C.Both the material amount of income resulting from the liquidation of LIFO inventory, and the amount of any reversal of any write-down that is recognized as a reduction in cost of goods sold in the period解释:

Solution-

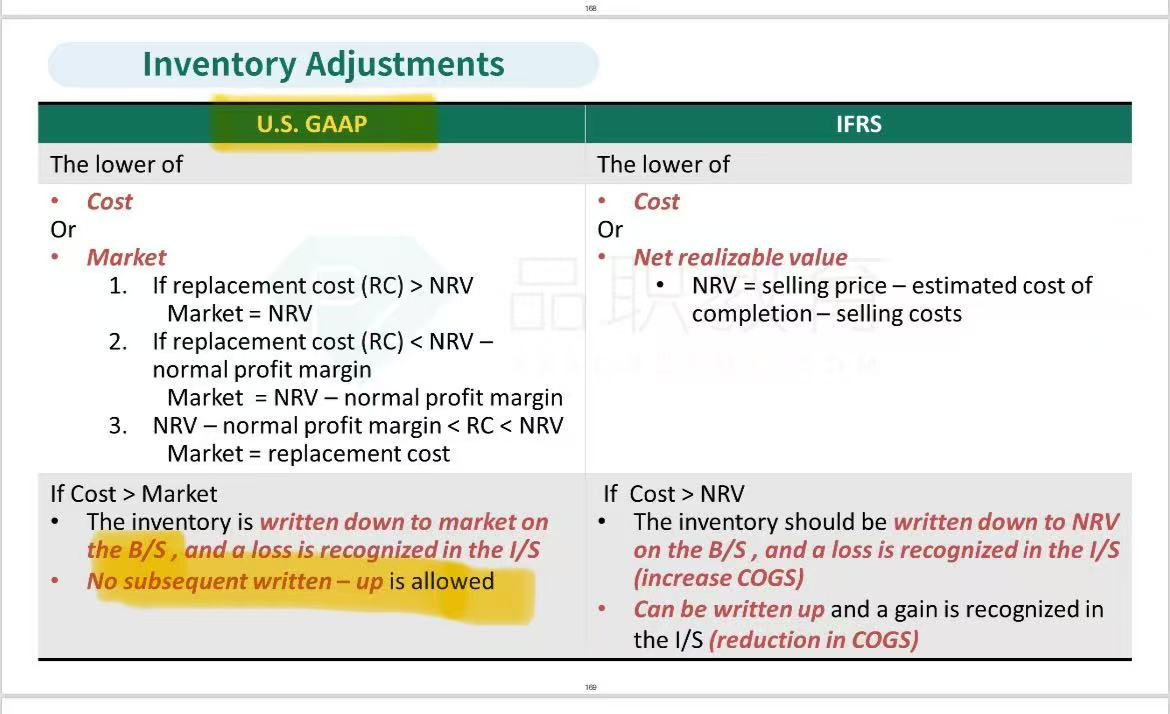

Correct because disclosures are useful when analyzing a company. IFRS requires eight financial statement disclosures concerning inventory, three of which are:

- the accounting policies adopted in measuring inventories, including the cost formula (inventory valuation method) used;

- the amount of any reversal of any write-down that is recognised as a reduction in cost of sales in the period;

- the circumstances or events that led to the reversal of a write-down of inventories.

Inventory-related disclosures under US GAAP are very similar to the disclosures above, except that requirements for the second and third are not relevant because US GAAP do not permit the reversal of prior-year inventory write-downs. US GAAP also require disclosure of significant estimates applicable to inventories and of any material amount of income resulting from the liquidation of LIFO inventory.

-

Incorrect because disclosures are useful when analyzing a company. IFRS requires eight financial statement disclosures concerning inventory, three of which are:

- the accounting policies adopted in measuring inventories, including the cost formula (inventory valuation method) used;

- the amount of any reversal of any write-down that is recognised as a reduction in cost of sales in the period;

- the circumstances or events that led to the reversal of a write-down of inventories.

Inventory-related disclosures under US GAAP are very similar to the disclosures above, except that requirements for the second and third are not relevant because US GAAP do not permit the reversal of prior-year inventory write-downs. US GAAP also require disclosure of significant estimates applicable to inventories and of any material amount of income resulting from the liquidation of LIFO inventory.

-

Incorrect because disclosures are useful when analyzing a company. IFRS requires eight financial statement disclosures concerning inventory, three of which are:

- the accounting policies adopted in measuring inventories, including the cost formula (inventory valuation method) used;

- the amount of any reversal of any write-down that is recognised as a reduction in cost of sales in the period;

- the circumstances or events that led to the reversal of a write-down of inventories.

Inventory-related disclosures under US GAAP are very similar to the disclosures above, except that requirements for the second and third are not relevant because US GAAP do not permit the reversal of prior-year inventory write-downs. US GAAP also require disclosure of significant estimates applicable to inventories and of any material amount of income resulting from the liquidation of LIFO inventory.

•

Solution

- Correct because disclosures are useful when analyzing a company. IFRS requires eight financial statement disclosures concerning inventory, three of which are:

- the accounting policies adopted in measuring inventories, including the cost formula (inventory valuation method) used;

- the amount of any reversal of any write-down that is recognised as a reduction in cost of sales in the period;

- the circumstances or events that led to the reversal of a write-down of inventories.

- Inventory-related disclosures under US GAAP are very similar to the disclosures above, except that requirements for the second and third are not relevant because US GAAP do not permit the reversal of prior-year inventory write-downs. US GAAP also require disclosure of significant estimates applicable to inventories and of any material amount of income resulting from the liquidation of LIFO inventory.

- Incorrect because disclosures are useful when analyzing a company. IFRS requires eight financial statement disclosures concerning inventory, three of which are:

- the accounting policies adopted in measuring inventories, including the cost formula (inventory valuation method) used;

- the amount of any reversal of any write-down that is recognised as a reduction in cost of sales in the period;

- the circumstances or events that led to the reversal of a write-down of inventories.

- Inventory-related disclosures under US GAAP are very similar to the disclosures above, except that requirements for the second and third are not relevant because US GAAP do not permit the reversal of prior-year inventory write-downs. US GAAP also require disclosure of significant estimates applicable to inventories and of any material amount of income resulting from the liquidation of LIFO inventory.

- Incorrect because disclosures are useful when analyzing a company. IFRS requires eight financial statement disclosures concerning inventory, three of which are:

- the accounting policies adopted in measuring inventories, including the cost formula (inventory valuation method) used;

- the amount of any reversal of any write-down that is recognised as a reduction in cost of sales in the period;

- the circumstances or events that led to the reversal of a write-down of inventories.

- Inventory-related disclosures under US GAAP are very similar to the disclosures above, except that requirements for the second and third are not relevant because US GAAP do not permit the reversal of prior-year inventory write-downs. US GAAP also require disclosure of significant estimates applicable to inventories and of any material amount of income resulting from the liquidation of LIFO inventory.

Analysis of Inventories