Bryan Yee is a junior analyst at HK Partners, a leading asset manager in Hong Kong. His boss, Brittany Chen, has asked Yee to assist her in analyzing eLeisure, a leading firm in the travel and leisure industry. eLeisure operates an online travel agency in Asia that provides travel products and services to travelers and travel agents. Chen provides Yee with a list of questions to help her finalize her analysis of discount rates as they pertain to the valuation of eLeisure, compare the firm with its industry, and determine intrinsic value estimates for eLeisure’s common stock.

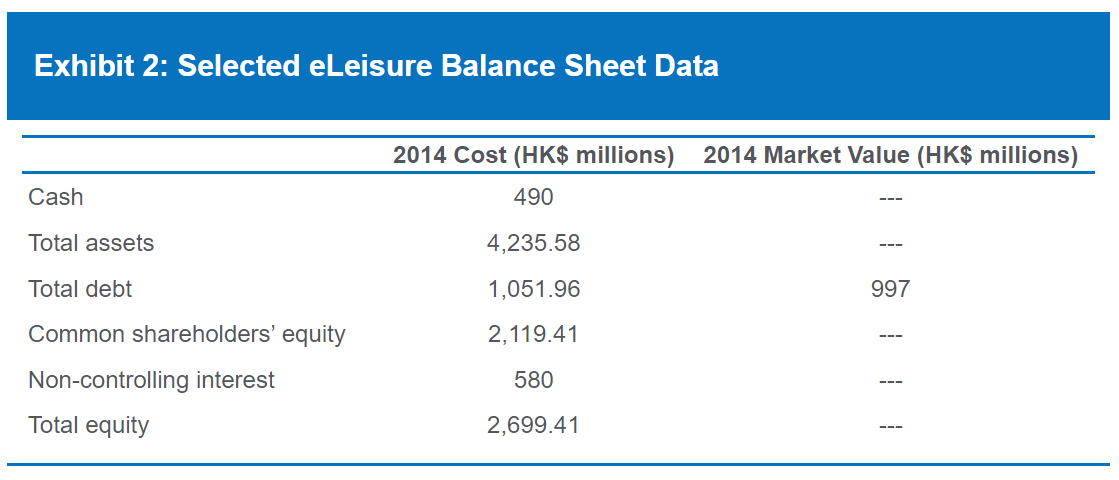

Chen first asks Yee to estimate eLeisure’s sustainable growth rate, which he does using the using the information in Exhibits 1 and 2.

The current share price of eLeisure’s common equity is HK$31.28. Chen mentions to Yee that historically, the company has had a ratio of enterprise value (EV) to sales of 1.25×. She asks Yee to use the information in Exhibits 1 and 2 along with this metric to determine whether eLeisure’s common shares are appropriately priced.

Chen asks Yee to refine his analysis of the dividend growth rate and discount rates to value eLeisure’s equity. Yee looks at eLeisure in more detail and concludes that its expansion potential will likely follow three distinct stages of growth, provided in Exhibit 3. He also determines the long-term return on equity (ROE) for the stock and its required rate of return, which are also presented in Exhibit 3.

With these estimates, Yee determines the intrinsic value of eLeisure common stock using the dividend discount model (DDM).

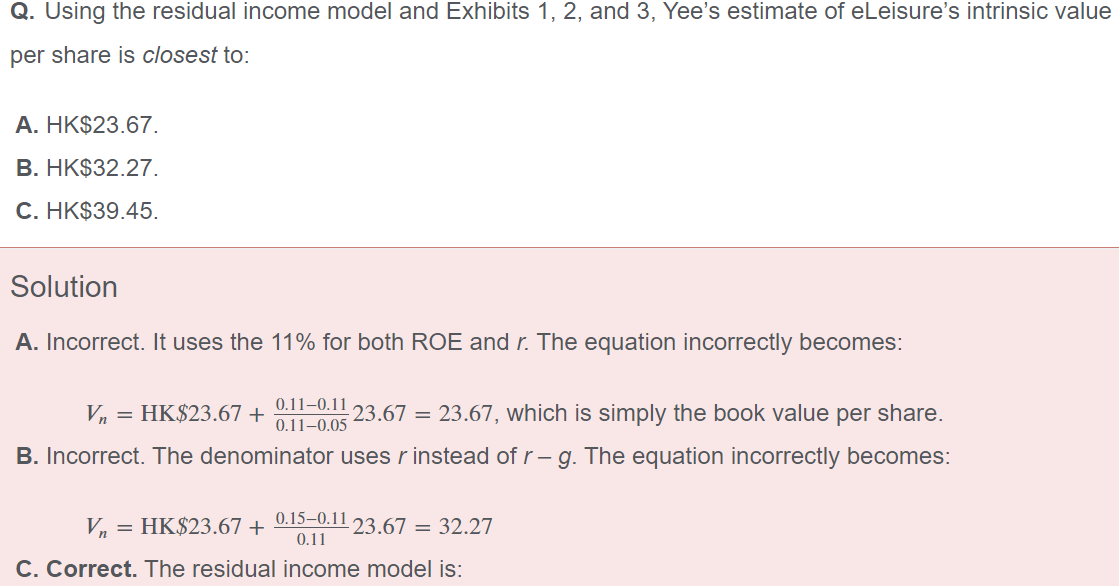

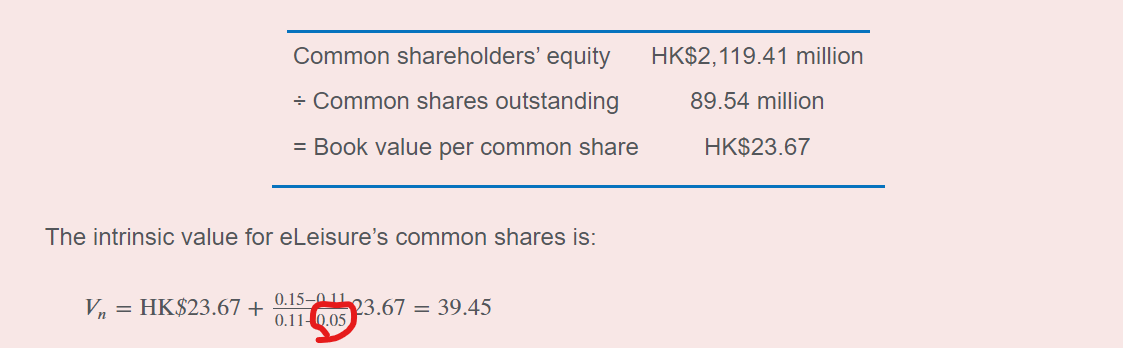

Chen next instructs Yee to minimize the uncertainty in making assumptions about eLeisure’s future earnings and long-term dividend growth by using the residual income model. Yee uses the data in Exhibits 1, 2, and 3 to calculate eLeisure's intrinsic value per common share.

Yee discusses with Chen the best reasons for using the residual income model and provides the following explanation:

“The residual income model’s strengths include the fact that it uses readily available accounting data and focuses on economic profitability. Weaknesses include the fact that accounting data can be manipulated by management, the cost of debt capital is assumed to be reflected by interest expense, and terminal values make up a large portion of the value of a firm’s equity.”

Several firms in the leisure industry in Asia are privately held. Chen asks Yee to provide three key differences between valuing private and public companies. He cites the following differences:

- Private firms are generally smaller than public firms. Being smaller, they can have enhanced growth prospects because of easier access to growth capital.

- Agency issues are usually greater at private companies.

- Small companies might decide to remain privately held because higher compliance costs may outweigh any other benefits of being public.

Question

请问答案里的这个g=0.05是怎么来的?为什么要用第三阶段的g去计算?之前别人提问时,有Maggie老师回答说“倒推”,但没说怎么倒推。我试了两种倒推,都推不到0.05。所以不知这位老师是怎么倒推出0.05的。谢谢!