NO.PZ2023101902000055

问题如下:

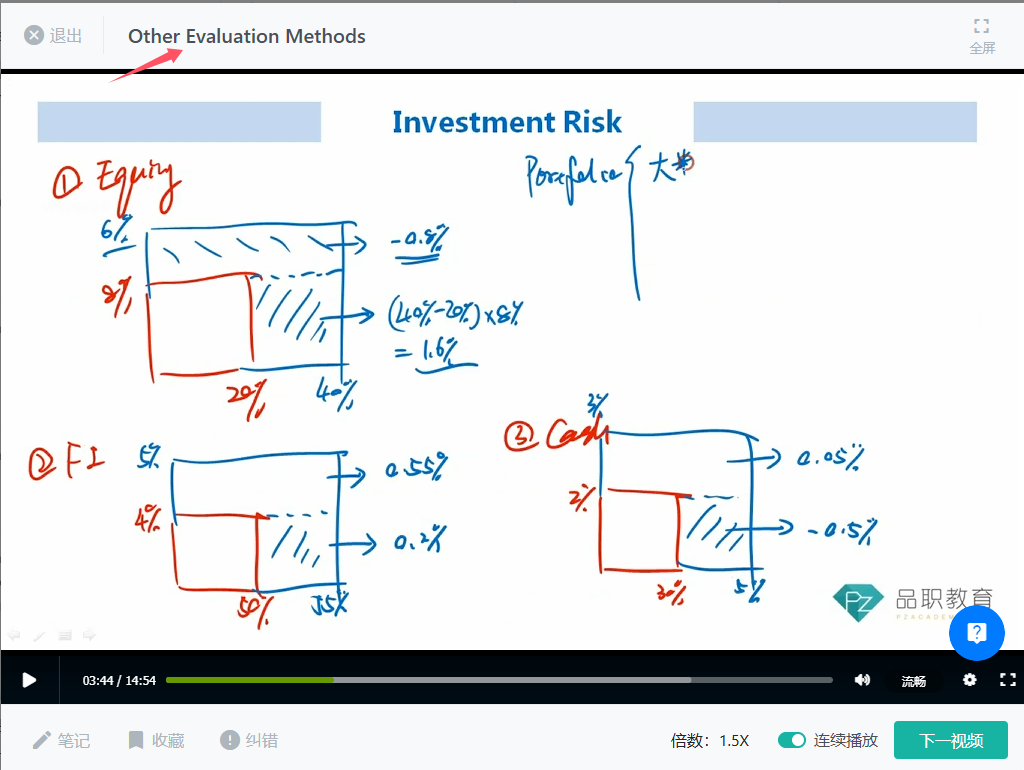

A risk manager runs a performance attribution analysis on an actively managed portfolio using a selected benchmark. The weights and performance of the different market sectors within the portfolio and the benchmark are given below:

What conclusion can be drawn from the data above by using common performance attribution analysis?

选项:

A.The portfolio outperforms the benchmark primarily because of the contribution of asset allocation. B.The portfolio outperforms the benchmark primarily because of the contribution of security selection within market sectors. C.The portfolio underperforms the benchmark primarily because of the contribution of asset allocation. D.The portfolio underperforms the benchmark primarily because of the contribution of security selection within market sectors.解释:

三个维度,porfolio都差不多输给了benchmark啊

麻烦详细讲解下