NO.PZ2023100905000020

问题如下:

A risk analyst at a fundmanagement company is discussing with the risk team the gaps in the company’s riskmeasurement system. Among the issues they have identified is the understandingthat failing to anticipate cash flow needs is one of the most serious errorsthat a firm can make. Addressing such a problem demands that a goodliquidity-at-risk(LaR) measurement system be an essential part of the bank'srisk management framework.

Which of thefollowing statements concerning LaR is correct? (Practice Exam)

选项:

A.

A firm's LaR tends to decrease as its credit quality declines.

B.

For a hedged portfolio, the LaR can differ significantly from the VaR.

C.

Hedging using futures has the same impact on LaR as hedging using long option positions.

D.

Reducing the basis risk through hedging decreases LaR

解释:

Explanation:The LaR candiffer substantially from the VaR in a hedged portfolio, and in differentsituations can be larger or smaller than the VaR. For example, consider aportfolio where futures contracts are used to hedge. While the hedge can reducethe VaR of the portfolio, the LaR can be larger than the VaR as the futurescontracts create an exposure to margin calls and the potential for cashoutflows. Alternatively, in situations where the hedging instruments do notresult in potential cash outflows over the measurement period (e.g. a portfolioof European options which do not expire during the period), the LaR can besmaller than the VaR.

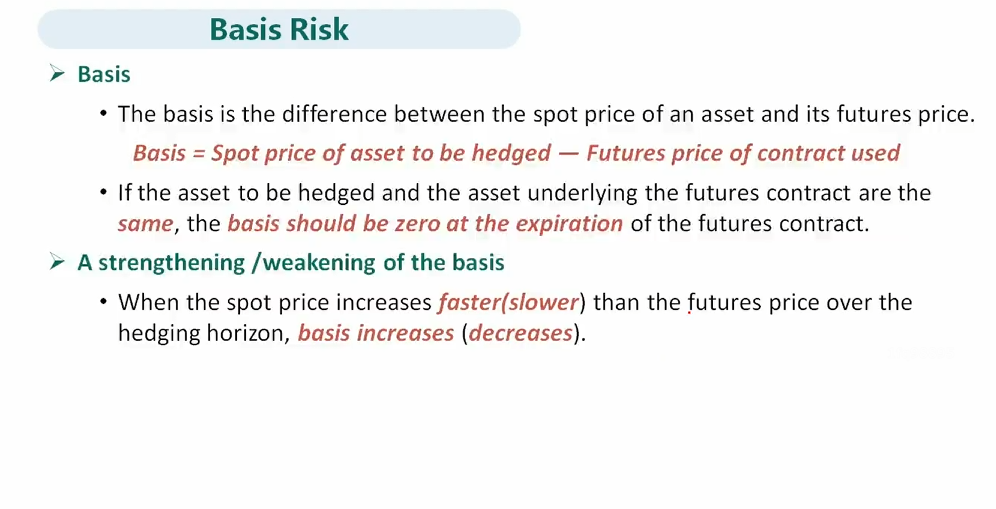

basis risk是什么,对LaR的影响是怎么样的