NO.PZ2023101902000046

问题如下:

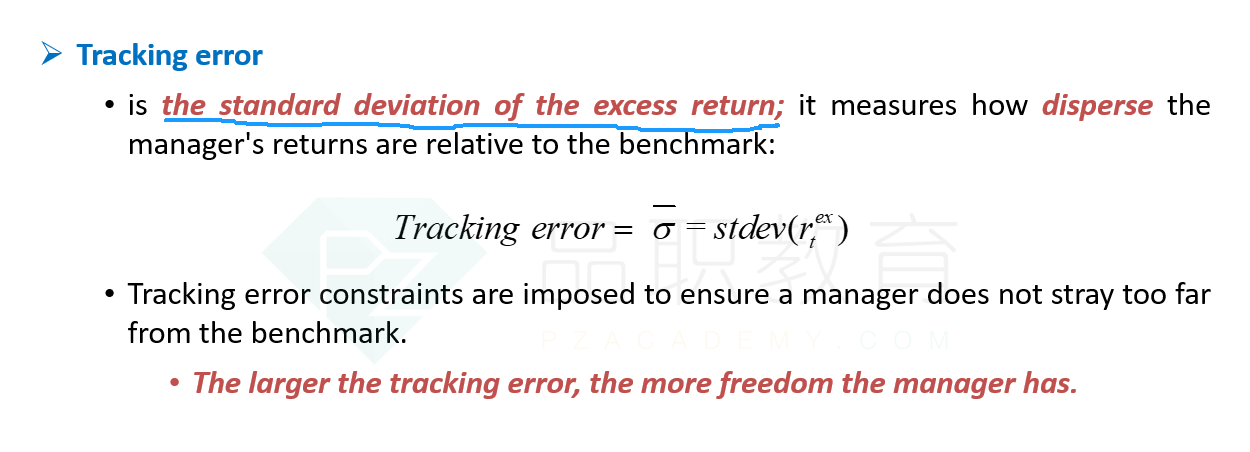

A fund manager recently received a report on the performance of his portfolio over the last year. According to the report, the portfolio return is 9.3%, with a standard deviation of 13.5%, and beta of 0.83. The risk-free rate is 3.2%, the semi-standard deviation of portfolio is 8.4%, and the tracking error of the portfolio to the benchmark index is 2.8%. What is the difference between the value of the fund’s sortino ratio (computed relative to the risk-free rate) and its Sharpe ratio?选项:

A.1.727 B.0.274 C.-0.378 D.0.653解释:

Sharp ratio = (9.3% - 3.2%)/13.5% = 0.4519, Sortino ratio = (9.3% - 3.2%)/8.4% = 0.7262, so Sortino ratio - sharp ratio = 0.274如题