NO.PZ2024042601000111

问题如下:

Setting margin levels and loss reserves are important aspects of mitigating systemic risk through the use of a central counterparty (CCP). Which of the following statements most accurately reflects the calculation of initial margins?

选项:

A.

The value at risk (VaR) approach sets appropriate initial margins at the 99% confidence level

B.

The Standard Portfolio Analysis of Risk (SPAN) is considered the most advanced methodology today in calculating initial margins

C.

The calculation of the initial margin should be based on volatility, tail risk, and dependency

D.

Initial margins depend solely on the credit quality of the clearing member

解释:

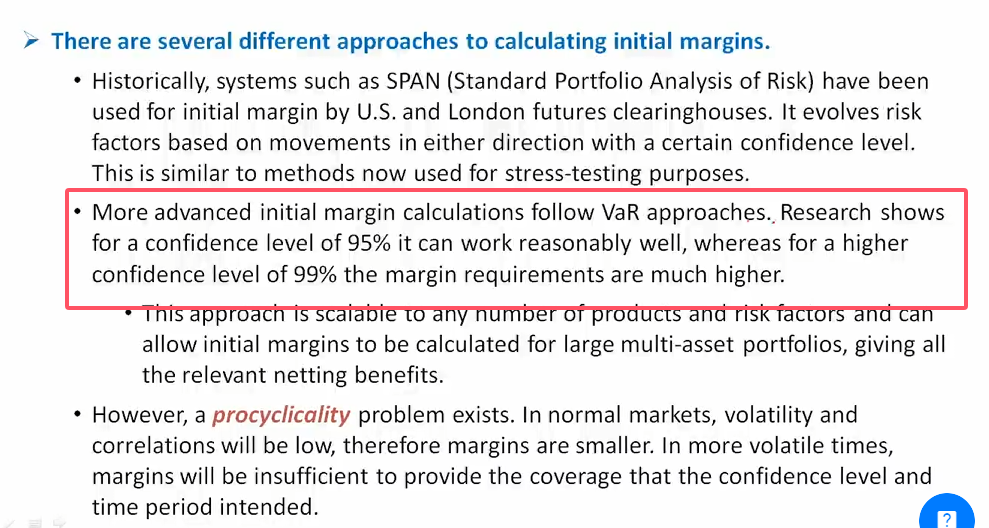

The calculation of the initial margin should be based on volatility, tail risk, and dependency. The value at risk (VaR) approach is a more advanced method than the SPAN approach for calculating initial margins. Studies suggest that the VaR approach does a good job of setting initial margins at the 95% confidence level, but at the 99% confidence level initial margins are not sufficient. The initial margin depends primarily on market risk and not the credit quality of the clearing member.

initial margin不是cover 99%情况下的最大损失吗