NO.PZ2023091901000028

问题如下:

Two risk analysts are discussing the efficient frontier following a presentation on the different measures of financial risk. According to the CAPM, which of the following statements is correct with respect to the efficient frontier?

选项:

A.

The capital market line always has a positive slope and its steepness depends on the market risk premium and the volatility of the market portfolio.

B.

The capital market line is the straight line connecting the risk-free asset with the zero beta minimum variance portfolio

C.

Investors with the lowest risk aversion will typically hold the portfolio of risky assets that has the lowest standard deviation on the efficient frontier.

D.

The efficient frontier allows different individuals to have different portfolios of risky assets based upon their individual forecasts for asset returns

解释:

Explanation: The capital market line connects the risk-free asset with the market portfolio, which is the efficient portfolio at which the capital market line is tangent to the efficient frontier. The equation of the capital market line is as follows:

where the subscript e denotes an efficient portfolio. Since the shape of the efficient frontier is dictated by the market risk premium, RM-RF, and the volatility of the market, the slope of the capital market line will also be dependent on these two factors.

资本市场线连接无风险资产和市场投资组合,这是资本市场线与有效边界相切的有效投资组合。

资本市场线的方程为:

其中下标e表示有效投资组合。

由于有效边界的形状是由市场风险溢价、RM-RF和市场波动性决定的,所以资本市场线的斜率也将取决于这两个因素。

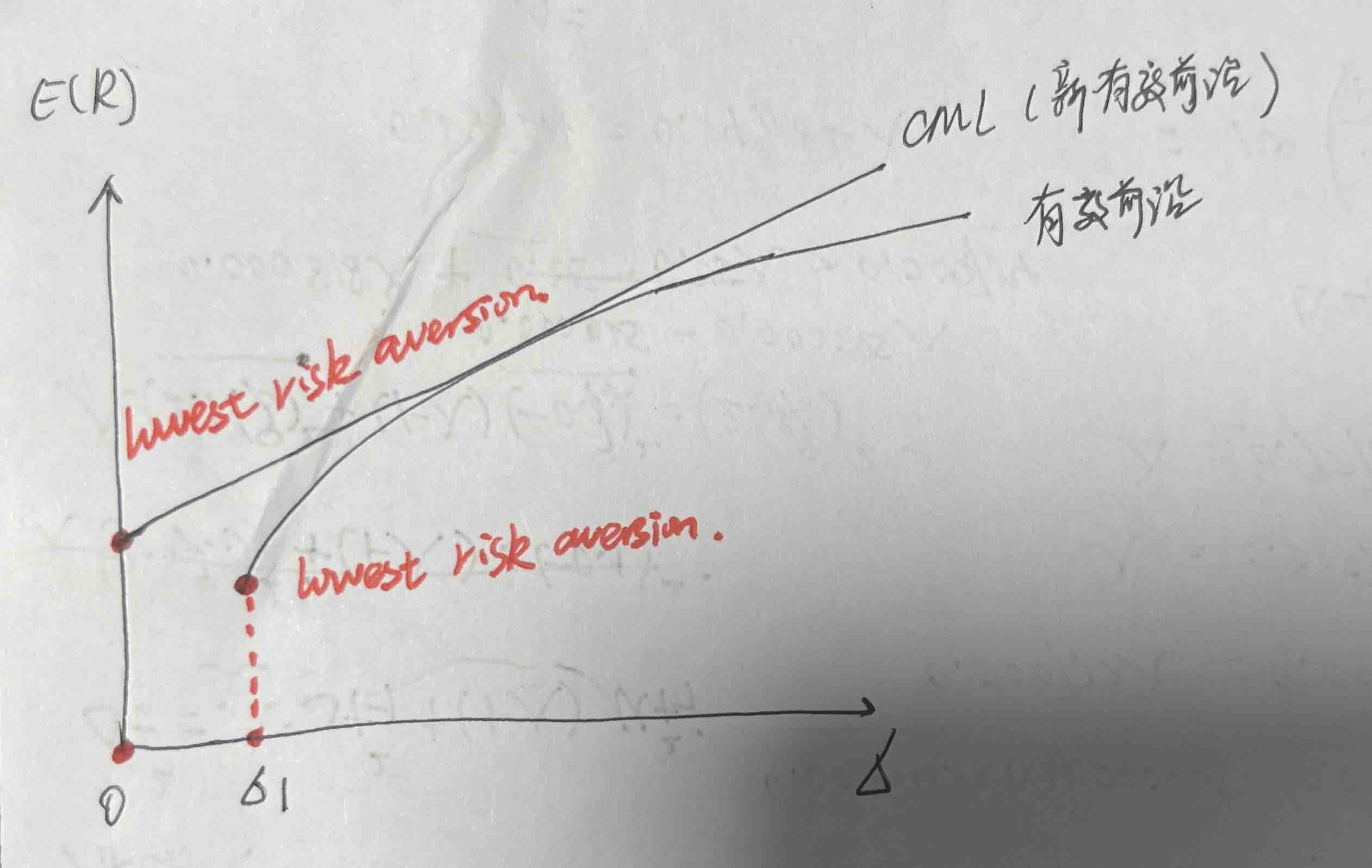

C选项有一点不明白,如果是CML,风险最厌恶,也就是下面图的红色点,不也是最小方差的点吗?