NO.PZ202308140300007606

问题如下:

Robert Groff, an equity analyst, is preparing a report on Crux Corp. As part of his report, Groff makes a comparative financial analysis between Crux and its two main competitors, Rolby Corp. and Mikko Inc. Crux and Mikko report under US GAAP and Rolby reports under IFRS.

Groff gathers information on Crux, Rolby, and Mikko. The relevant financial information on the three companies, and on the industry, is provided in Exhibit 1.

Exhibit 1:

Selected Financial Information (millions of US dollars)

* This does not match the change in the inventory valuation allowance because the valuation allowance is reduced to reflect the valuation allowance attached to items sold and increased for additional necessary write-downs.

To compare the financial performance of the three companies, Groff decides to convert LIFO figures into FIFO figures, and adjust figures to assume no valuation allowance is recognized by any company.

选项:

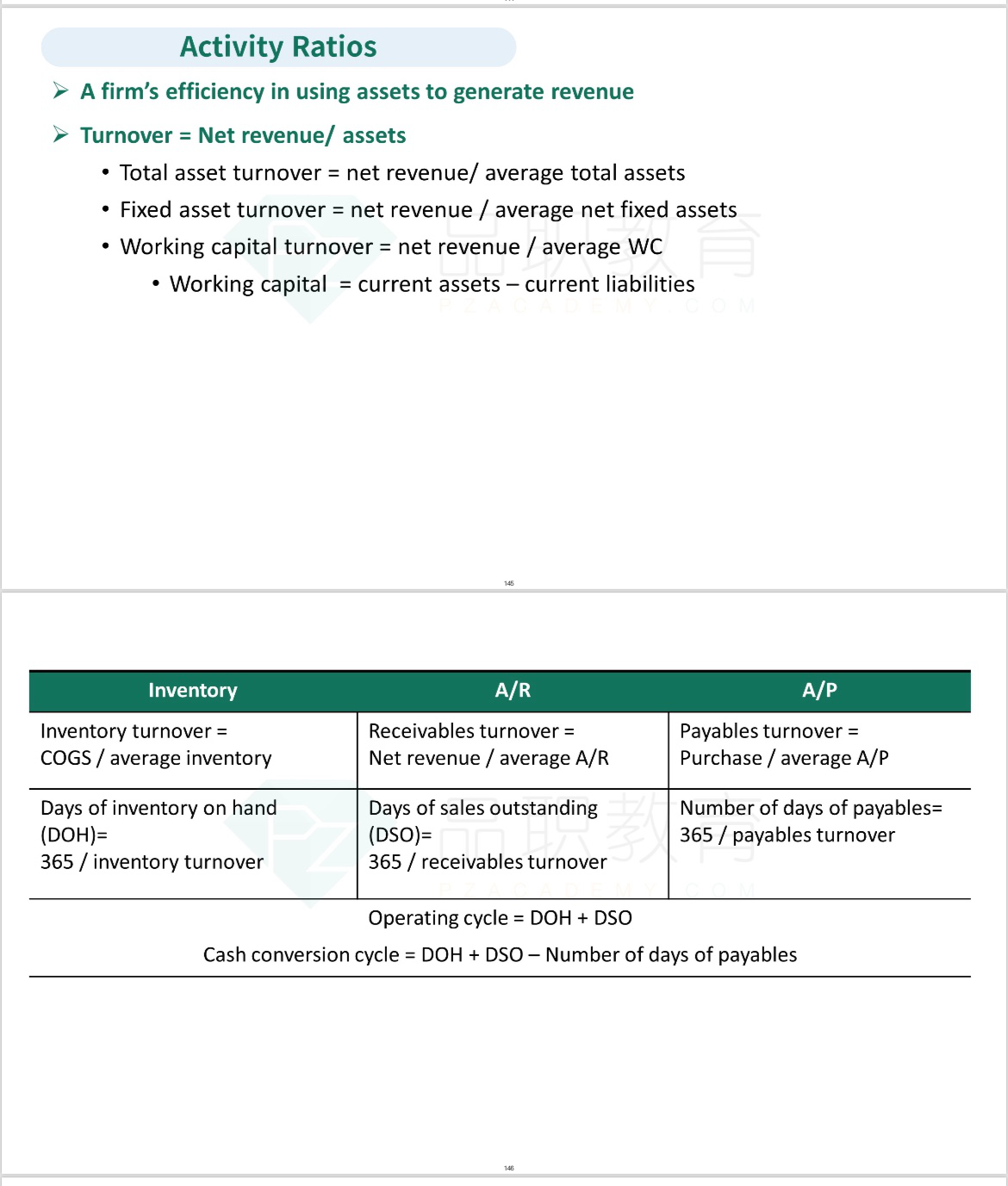

A.Activity ratios B.Solvency ratios C.Profitability ratios解释:

A is correct. An inventory write-down increases the cost of sales and reduces profit and reduces the carrying value of inventory and assets. This has a negative effect on profitability and solvency ratios. However, activity ratios appear positively affected by a write-down because the asset base, whether total assets or inventory (denominator), is reduced. The numerator, sales, in total asset turnover is unchanged, and the numerator, cost of sales, in inventory turnover is increased. Thus, turnover ratios are higher and appear more favorable as the result of the write-down.

如题