NO.PZ2024070101000002

问题如下:

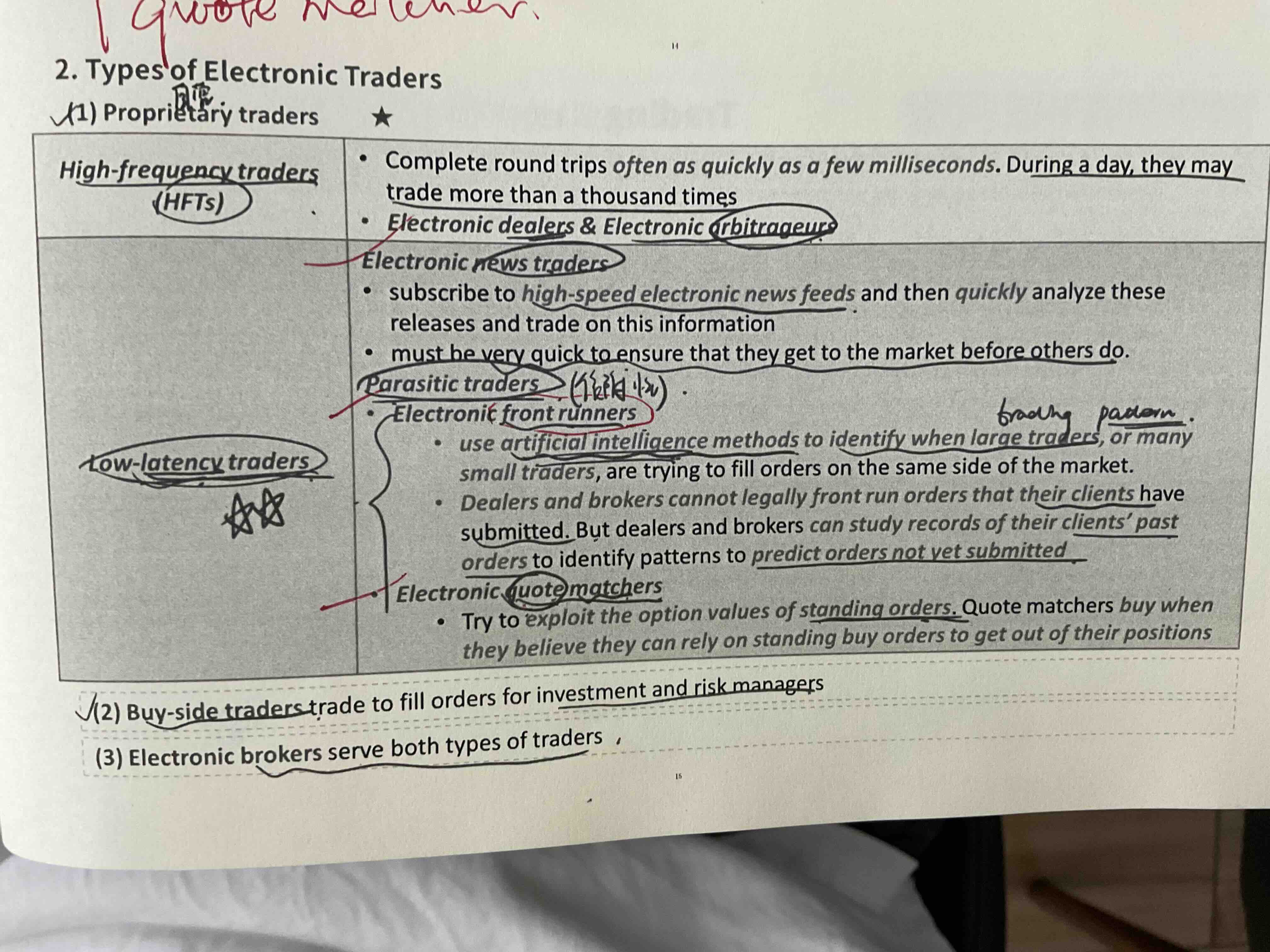

Davis knows investment committee members often worry about TitanCorp’s ability to purchase large quantities of stock. Low-latency traders try to profit by identifying the intentions of institutional investors. Davis adds a section to the presentation explaining how TitanCorp’s traders counter low-latency traders. They break up purchase orders and randomize the timing and sizes of these purchases.

Davis's explanation of TitanCorp traders' practices is most likely describing an attempt to counter the efforts of:

选项:

A.

proprietary traders.

B.

quote matchers.

C.

dealers.

解释:

B is correct. Quote matchers are parasitic traders who base their predictions about future prices on information they obtain about orders that other traders intend to fill. Buy-side traders and their brokers are aware of the efforts quote matchers make to detect and front-run their orders. Accordingly, they submit orders at random times and in various sizes in order to make detection more difficult.

A is incorrect. Electronic proprietary traders can include high-frequency traders who complete round trips of a purchase followed by a sale within a short period of time and news traders who trade quickly in response to new information. They would generally not have the same interests as parasitic traders.

C is incorrect. Electronic dealers make markets by placing bids and offers with the expectation that they can profit from round trips at favorable net spreads. On the first indication that prices may move against their inventory positions, they immediately take steps to reduce their exposure.

为啥不选a a不是包括了front runner吗