NO.PZ2022062760000013

问题如下:

An analyst is testing a hypothesis that the beta, 𝛽, of stock CDM is 1. The analyst runs an ordinary least squares

regression of the monthly returns of CDM, RCDM, on the monthly returns of the S&P 500 Index, Rm, and obtains

the following relation:

The analyst also observes that the standard error of the coefficient of Rm is 0.80. In order to test the

hypothesis H0: 𝛽 = 1 against H1: 𝛽 ≠ 1, what is the correct statistic to calculate?

选项:

A.t-statistic

Chi-squared test statistic

Jarque-Bera test statistic

Sum of squared residuals

解释:

中文解析:

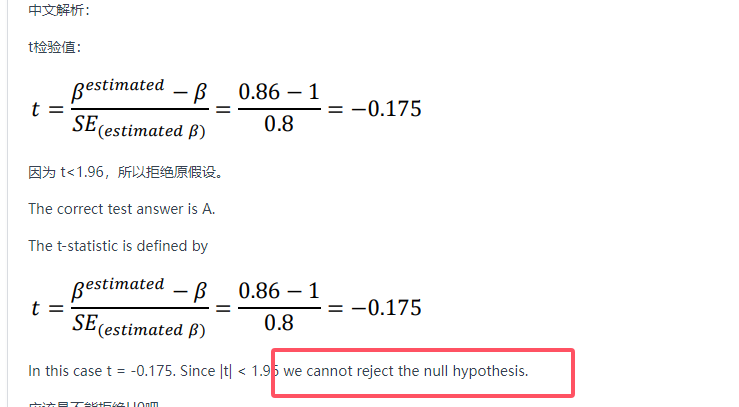

t检验值:

因为 t<1.96,所以拒绝原假设。

The correct test answer is A.

The t-statistic is defined by

In this case t = -0.175. Since |t| < 1.96 we cannot reject the null hypothesis.

应该是不能拒绝H0吧