NO.PZ2023100703000087

问题如下:

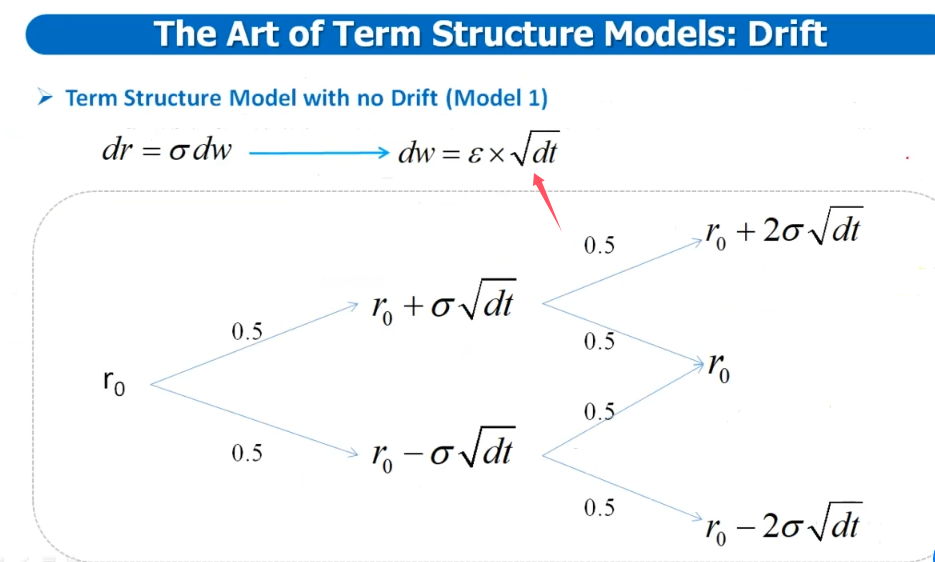

Model 1 has a no-drift assumption. Using this model, if the current short-term interest rate is 6%, annual volatility is 100bps, and dw is a normally distributed random variable with mean equals zero and standard deviation of zero as its expected value. One month later, the realization of dw is -0.4. What is the change in the spot rate and the new spot rate?选项:

A.0.40% -6.40% B.-0.40% 5.60% C.0.80% 6.80% D.-0.80% 5.20%解释:

dr = σ dw dr = 1% x (-0.4) = -0.4% = -40 basis points Since the initial rate was 6% and dr = -0.40%, the new spot rate in one month is: 6% - 0.40% = 5.60%题干所有数据都是年化的,但给dw的说法是1个月后dw=-0.4。麻烦解释一下为什么不需要月化?谢谢