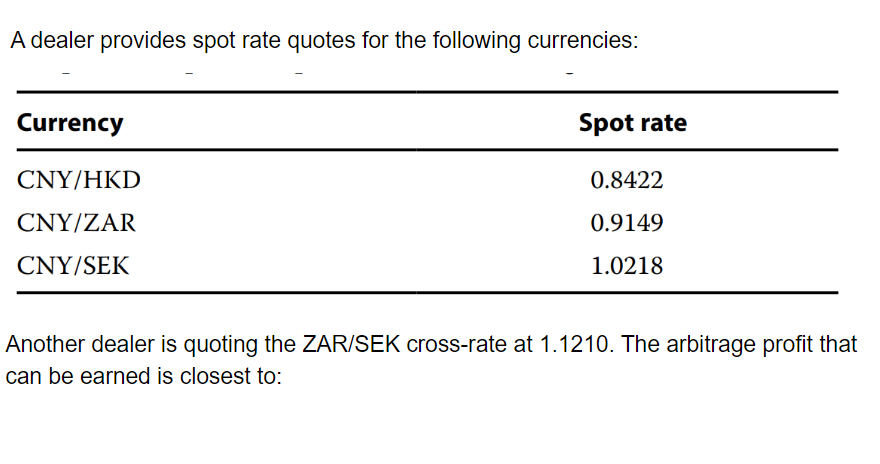

NO.PZ2023061903000022 问题如下 A aler provis spot rate quotes for the following currencies:Another aler is quoting the ZAR/SEK cross-rate 1.1210. The arbitrage profit thcearneis closest to: A.ZAR3671 per million Swesh krona tra B.SEK4200 per million South Africrantra C.ZAR4200 per million Swesh krona tra C is correct. The ZAR/SEK cross-rate from the originaler is (1.0218/0.9149) = 1.1168, whiis lower ththe quote from the seconaler. To earn arbitrage profit, a currentrar woulbuy Swesh krona (sell South Africran from the originaler ansell Swesh krona (buy South Africran to the seconaler. On SEK1 million, the profit woulbe:SEK1,000,000 × (1.1210 – 1.1168) = ZAR4,200 C正确。初始交易商的ZAR/SEK交叉汇率为(1.0218/0.9149)= 1.1168,低于第二家交易商的报价。为了赚取套利利润,货币交易者会从最初的交易商那里买入瑞典克朗(卖出南非兰特),然后将瑞典克朗(买入南非兰特)卖给第二个交易商。以1亿瑞典克朗计算,其利润为:SEK1,000,000 × (1.1210 – 1.1168) = ZAR4,200 要找ZAR/ZEK,为什么要用1.0218/0.9149, 而不是0。9149/1.0218

没有图片

题干错误 题干显示不完整。

NO.PZ2023061903000022 问题如下 Another aler is quoting the ZAR/SEK cross-rate 1.1210. The arbitrage profit thcearneis closest to: A.ZAR3671 per million Swesh krona tra B.SEK4200 per million South Africrantra C.ZAR4200 per million Swesh krona tra C is correct. The ZAR/SEK cross-rate from the originaler is (1.0218/0.9149) = 1.1168, whiis lower ththe quote from the seconaler. To earn arbitrage profit, a currentrar woulbuy Swesh krona (sell South Africran from the originaler ansell Swesh krona (buy South Africran to the seconaler. On SEK1 million, the profit woulbe:SEK1,000,000 × (1.1210 – 1.1168) = ZAR4,200 C正确。初始交易商的ZAR/SEK交叉汇率为(1.0218/0.9149)= 1.1168,低于第二家交易商的报价。为了赚取套利利润,货币交易者会从最初的交易商那里买入瑞典克朗(卖出南非兰特),然后将瑞典克朗(买入南非兰特)卖给第二个交易商。以1亿瑞典克朗计算,其利润为:SEK1,000,000 × (1.1210 – 1.1168) = ZAR4,200 这道题目我是从“another aler\"开始显示题干的,完整的题目请告知。谢谢!