NO.PZ2022122601000022

问题如下:

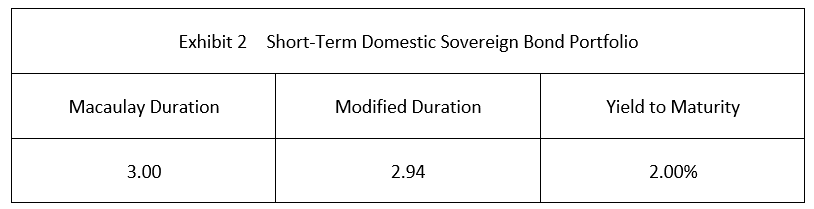

Martin asks the fixed-income portfolio manager to review the foundation’s bond portfolios. The existing aggregate bond portfolio is broadly diversified in domestic and international developed markets. The first segment of the portfolio to be reviewed is the domestic sovereign portfolio. The bond manager notes that there is a market consensus that the domestic yield curve will likely experience a single 20 bp increase in the near term as a result of monetary tightening and then remain relatively flat and stable for the next three years. Martin then reviews duration and yield measures for the short-term domestic sovereign bond portfolio in Exhibit 2.

Based on Exhibit 2 and the anticipated effects of the monetary policy change, the expected annual return over a three-year investment horizon will most likely be:

选项:

A.lower than 2.00% B.approximately equal to 2.00% C.greater than 2.00%

解释:

Correct Answer: B

If the investment horizon equals the (Macaulay) duration of the portfolio, the capital loss created by the increase in yields and the reinvestment effects (gains) will roughly offset, leaving the realized return approximately equal to the original yield to maturity. This relationship is exact if (a) the yield curve is flat and (b) the change in rates occurs immediately in a single step. In practice, the relationship is only an approximation. In the case of the domestic sovereign yield curve, the 20 bp increase in rates will likely be offset by the higher reinvestment rate, creating an annual return approximately equal to 2.00%.

中文解析:

如果投资期限等于投资组合的(麦考利)期限,则收益率增加所造成的资本损失和再投资效应(收益)将大致抵消,使实现回报大致等于原始到期收益率。如果(a)收益率曲线是平坦的,(b)利率的变化在单一步骤中立即发生,这种关系是准确的。在实践中,这种关系只是近似的。就国内主权债券收益率曲线而言,利率上升20个基点可能会被更高的再投资率所抵消,从而产生约等于2.00%的年回报率。