NO.PZ202208260100000708

问题如下:

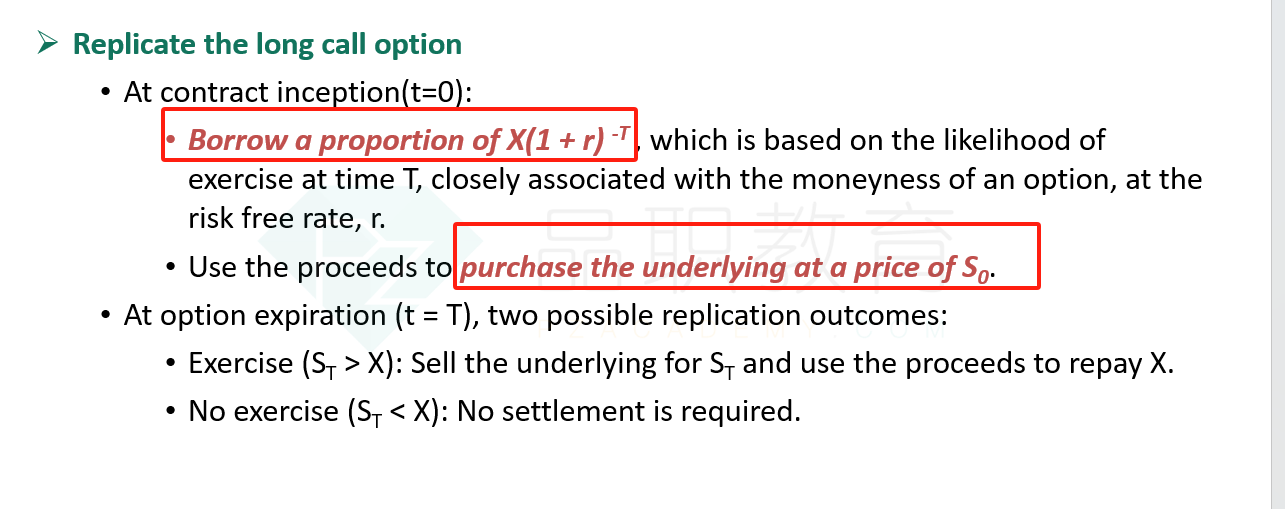

Which of the following statements correctly describes how VFO could replicate selling a call option on Biomian if exercise is certain?

选项:

A.Borrow X(1 + r)^-T at the risk-free rate and use the proceeds to buy Biomian stock at the current spot price, S0. At expiration, sell the Biomian stock and use the proceeds to pay off the loan.

B.Sell short Biomian stock at the current spot price, S0, and use the proceeds to lend X(1 + r)^-T at the risk-free rate. At expiration, receive X as repayment of the risk-free loan and buy back the Biomian stock.

C.Sell short Biomian stock at the current spot price, S0, and borrow X(1 + r)^-T at the risk-free rate. At expiration, pay off the risk-free loan of X and buy back the Biomian stock.

解释:

B is correct. To replicate selling a call option, combine shorting the underlying with risk-free lending. This is exactly the opposite strategy to replicate buying a call option in which the underlying is purchased with proceeds from risk-free borrowing. A is incorrect as this statement describes replicating buying a call option. C is incorrect as selling short and borrowing initially creates two cash inflows at t = 0 followed by two cash outflows at t = T.

题干意思是复制一个sell call吗?三个选项怎么理解?分别对应的啥?