NO.PZ2024021803000007

问题如下:

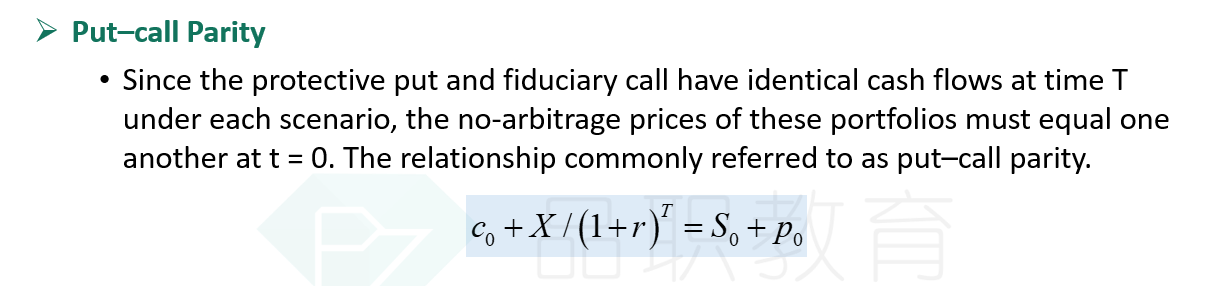

What is the equivalent portfolio to a European put option's payoff according to put-call parity?选项:

A.A long position in the underlying asset, a short call, and a long position in a risk-free bond. B.A short position in the underlying asset, a long call, and a long position in a risk-free bond. C.A short position in the underlying asset, a short call, and a short position in a risk-free bond.解释:

Put-call parity states that the payoff from holding a put and a risk-free bond (until option's maturity) is equivalent to holding a call and the underlying asset. 按照看涨看跌平价原理,持有一个看跌期权和到期无风险债券的收益相当于持有一个看涨期权和标的资产。What is the equivalent portfolio to a European put option's payoff according to put-call parity?

您的回答A, 正确答案是: B

A

不正确A long position in the underlying asset, a short call, and a long position in a risk-free bond.

B

A short position in the underlying asset, a long call, and a long position in a risk-free bond.

C

A short position in the underlying asset, a short call, and a short position in a risk-free bond.