NO.PZ202312260100000503

问题如下:

At the first swap settlement date, Beryl Hedge Fund would:

选项:

A.receive $12,000,000. B.receive $24,000,000. C.pay $24,000,000.解释:

On the first settlement date:

1. Beryl Hedge Fund would receive the agreed-upon floating interest rate in the swap contract and

2. Beryl Hedge Fund would pay any gains on the QQQ position or receive any negative returns on the QQQ position.

Notional amount of the swap = 40% of $500 million=$200 million

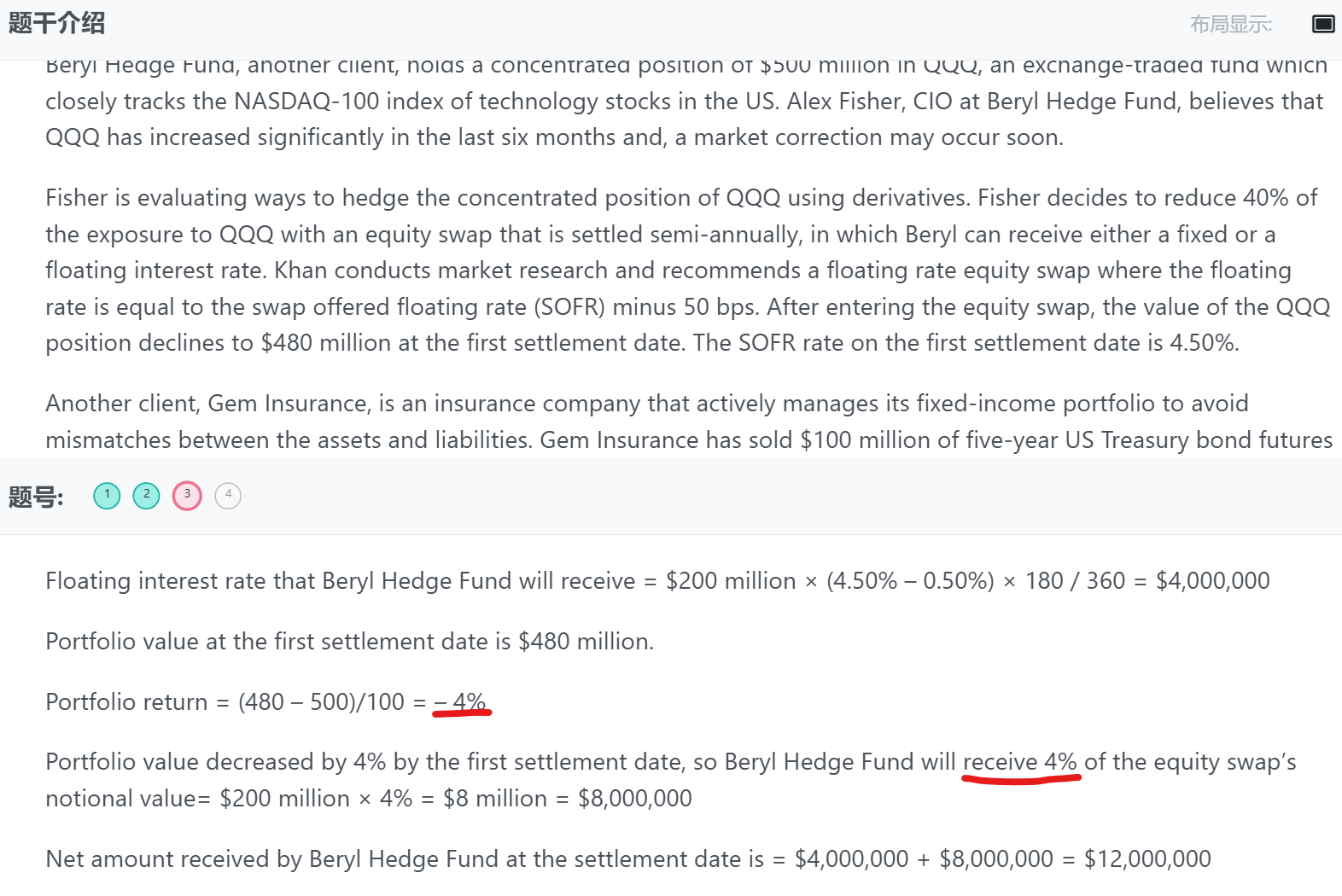

Floating interest rate that Beryl Hedge Fund will receive = $200 million × (4.50% – 0.50%) × 180 / 360 = $4,000,000

Portfolio value at the first settlement date is $480 million.

Portfolio return = (480 – 500)/100 = – 4%

Portfolio value decreased by 4% by the first settlement date, so Beryl Hedge Fund will receive 4% of the equity swap’s notional value= $200 million × 4% = $8 million = $8,000,000

Net amount received by Beryl Hedge Fund at the settlement date is = $4,000,000 + $8,000,000 = $12,000,000