NO.PZ202301280100000304

问题如下:

Which of David’s recommended strategies results in the

largest profit at expiration?

选项:

A.Strategy 1

Strategy 2

Strategy 3

解释:

Correct

Answer: C

Strategy 3

If the stock price

is $790, both puts expire worthless and the investor keeps the $22.08 credit

received per option plus any upside on the stock.

Any upside in the

stock price is protected as there are no short calls in this strategy.

Capital Gain

(unrealized) = 500,000 × ($790 – $750) = $20,000,000

Option Premia

Received = 500,000 × $31.31 = $15,655,000

Option Cost

Incurred = 500,000 × $9.23 = –$4,615,000

Profit =

$20,000,000 + $15,655,000 – $4,615,000 = $31,040,000

Ignoring the

increased value of the underlying, the profit from this option strategy alone =

$15,655,000 – $4,615,000 = $11,040,000

Strategy 1

If the stock price

is $790, the short calls are assigned and the investor will forgo all profits

above the strike price of $730.

Hence, any upside

in the stock price above $730 is nullified by the short $730 call.

Capital Loss

Incurred = 500,000 × ($790 – $750) = $20,000,000

Option Premia

Received = 500,000 × [$3.41 -(790-730)]= -$28,295,000

Profit = $20,000,000 - $28,295,000 = –$8,295,000

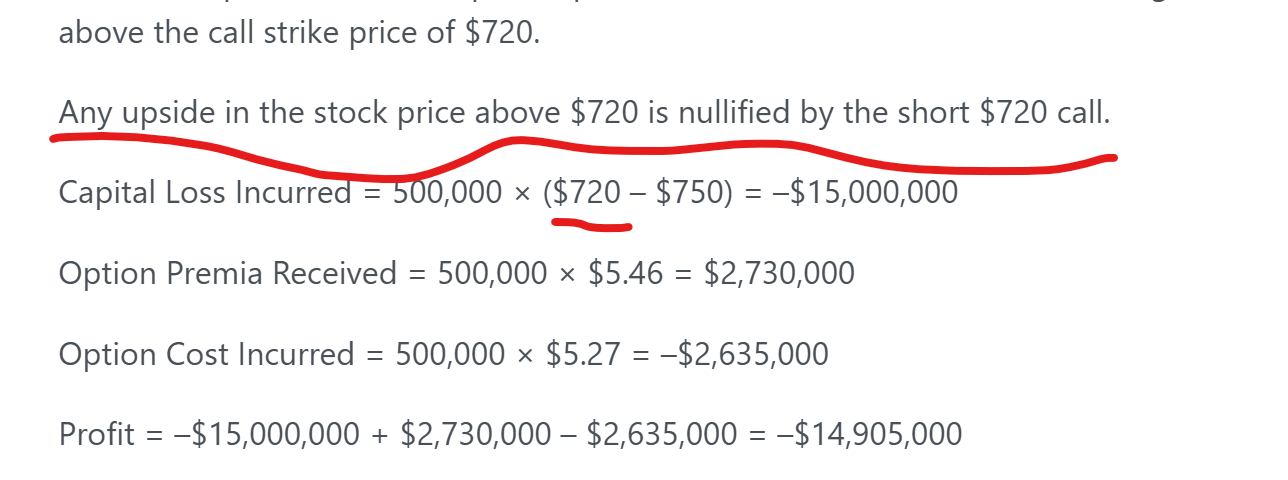

Strategy 2

If the stock price

is $790, the puts expire worthless and the short calls are assigned so the

investor will forgo all profits above the call strike price of $720.

Any upside in the

stock price above $720 is nullified by the short $720 call.

Capital Loss Incurred

= 500,000 × ($720 – $750) = –$15,000,000

Option Premia

Received = 500,000 × $5.46 = $2,730,000

Option Cost

Incurred = 500,000 × $5.27 = –$2,635,000

Profit =

–$15,000,000 + $2,730,000 – $2,635,000 = –$14,905,000