NO.PZ2023100703000106

问题如下:

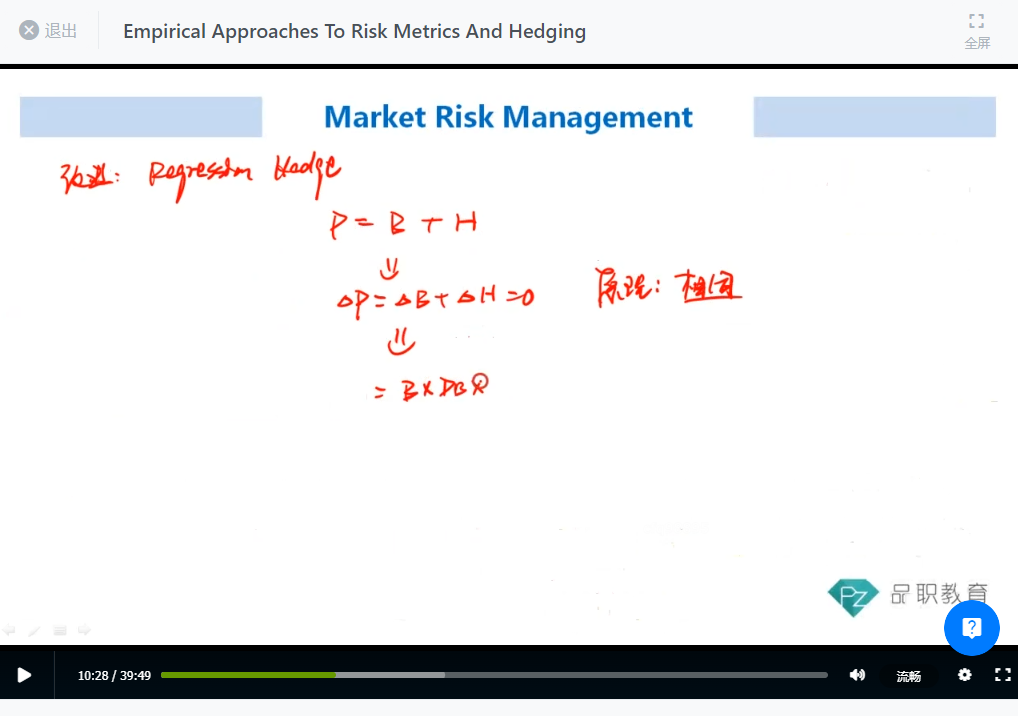

Gabrielle, a trader, is about to set up a regression hedge.She would sell $500,000 of a Treasury bond and purchase TIPS as a hedge. According to historical figures, the DV01on the T-bond is 0.085, the DV01on the TIPS is 0.063, and the regression beta coefficient (hedge adjustment factor) is 1.1. How much TIPS should Gabrielle purchase?选项:

A.336898 B.407647 C.613276 D.742063解释:

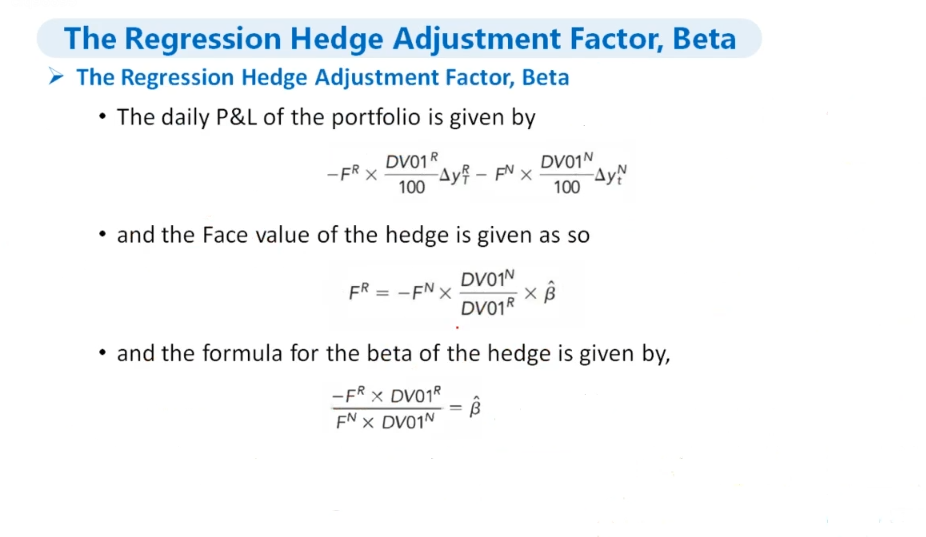

Defining FR and FN as the face amounts of the

real and nominal bonds, respectively, and their corresponding DV01s as DV01R

and DV01N, a DV01 hedge is adjusted by the hedge adjustment factor,

or beta, as follow:

这个beta 作为hedge instrument系数,为啥不是除以呢