NO.PZ2023100703000103

问题如下:

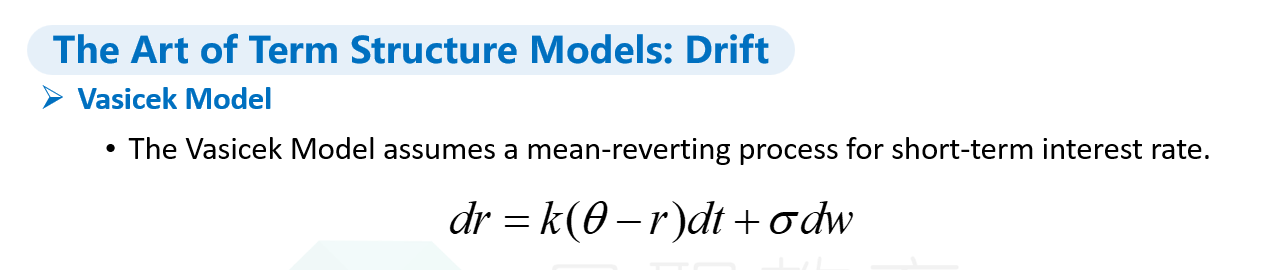

A quantitative analyst on the fixed-income desk of an investment bank is applying the Vasicek model to estimate future short-term interest rates. The model is given below: where dr is the change in the short-term interest rate, ϴ is the estimated long-run value of the short-term interest rate, k is the mean reversion rate, r is the current level of the short-term interest rate, σ is the annual basis-point volatility of the short-term interest rate, dt is the time interval measured in years, and dw is a normally distributed random variable with mean zero and standard deviation equal to the square root of dt. The analyst gathers the following information: • Current short-term interest rate (r): 3.35% • Long-run value of short-term interest rate (ϴ): 4.55% • Mean reversion rate (k): 0.06 • Annual basis-point volatility (σ): 120 bps The analyst then creates an interest rate tree, determines the expected short-term interest rate after 8 years, and calculates how long it will take the short-term interest rate to revert halfway to the long-run value. Which of the following statements would be correct for the analyst to make?选项:

A.The expected short-term interest rate is 3.81% and the half-life is 11.6 years. B.The expected short-term interest rate is 3.81% and the half-life is 16.7 years. C.The expected short-term interest rate is 4.09% and the half-life is 11.6 years. D.The expected short-term interest rate is 4.09% and the half-life is 16.7 years.解释:

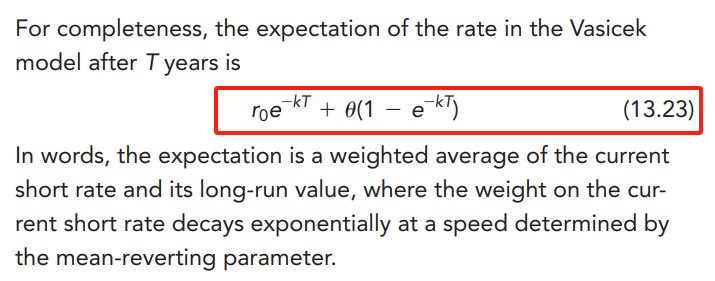

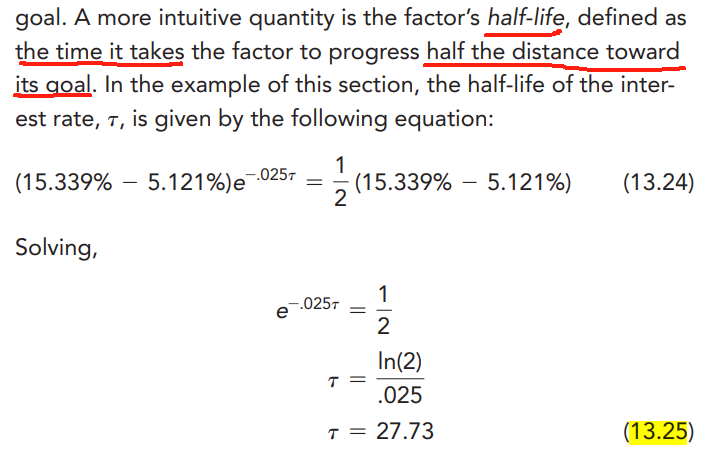

A is correct. The equation for determining the expected short-term interest rate after some number of years (T) when the interest rate process follows a Vasicek model is given as follows (equation 13.23 in the Market Risk book): r0*e-kT + ϴ*(1 - e-kT) Using the information provided, the expected short-term interest rate after 8 years is: 0.0335 * e-0.06*8 + 0.0455 * (1 - e-0.06*8) = 0.0335 * 0.6188 + 0.0455 * 0.3812 = 0.0381, 3.81%. The half-life of the short-term interest rate is given as being equal to ln(2)/k (see equation 13.25 in Market Risk book). Therefore, the half-life in this example is ln(2)/0.06 = 11.55 years. B is incorrect. The half-life is incorrectly calculated as being 1/k, or 1/0.06, 16.7 Years C is incorrect. The expected short-term interest rate is incorrectly estimated by switching the position of e-kT and 1 - e-kT, which then yields 4.09%. D is incorrect. Both errors made in B and C are made in this answer choice.感觉公式和Vmodel的公式写的不一样,具体解题思路求再讲一下