NO.PZ202305230100005406

问题如下:

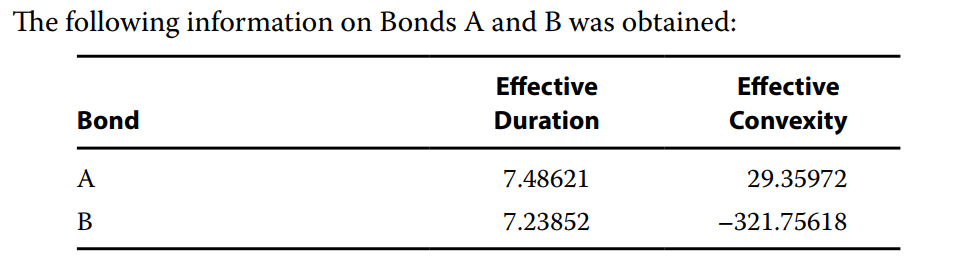

An investor’s well-diversified portfolio has $200,000 in cash. The investor aims to invest in short-term, one-year Large-Cap Company bonds, prior to using the cash to invest in an upcoming IPO. There are currently two Large-Cap Company bonds on the market to purchase, both with one-year maturities. One of the bonds, Bond A, is a non-callable bond, while Bond B is a callable bond. As a fixed-income analyst, you are asked to conduct an analysis.

The investor’s portfolio is diversified, and the fixed-income component of the portfolio has bonds of various maturities, with a duration of 7.48621. What would happen to the effective duration of the fixed-income component of the investor’s portfolio if Bond A is added to the portfolio?

选项:

A.It would increase.

It would decrease.

It would stay the same.

解释:

C is correct. Bond A has the same effective duration as the portfolio effective duration.

如题