NO.PZ2023091802000160

问题如下:

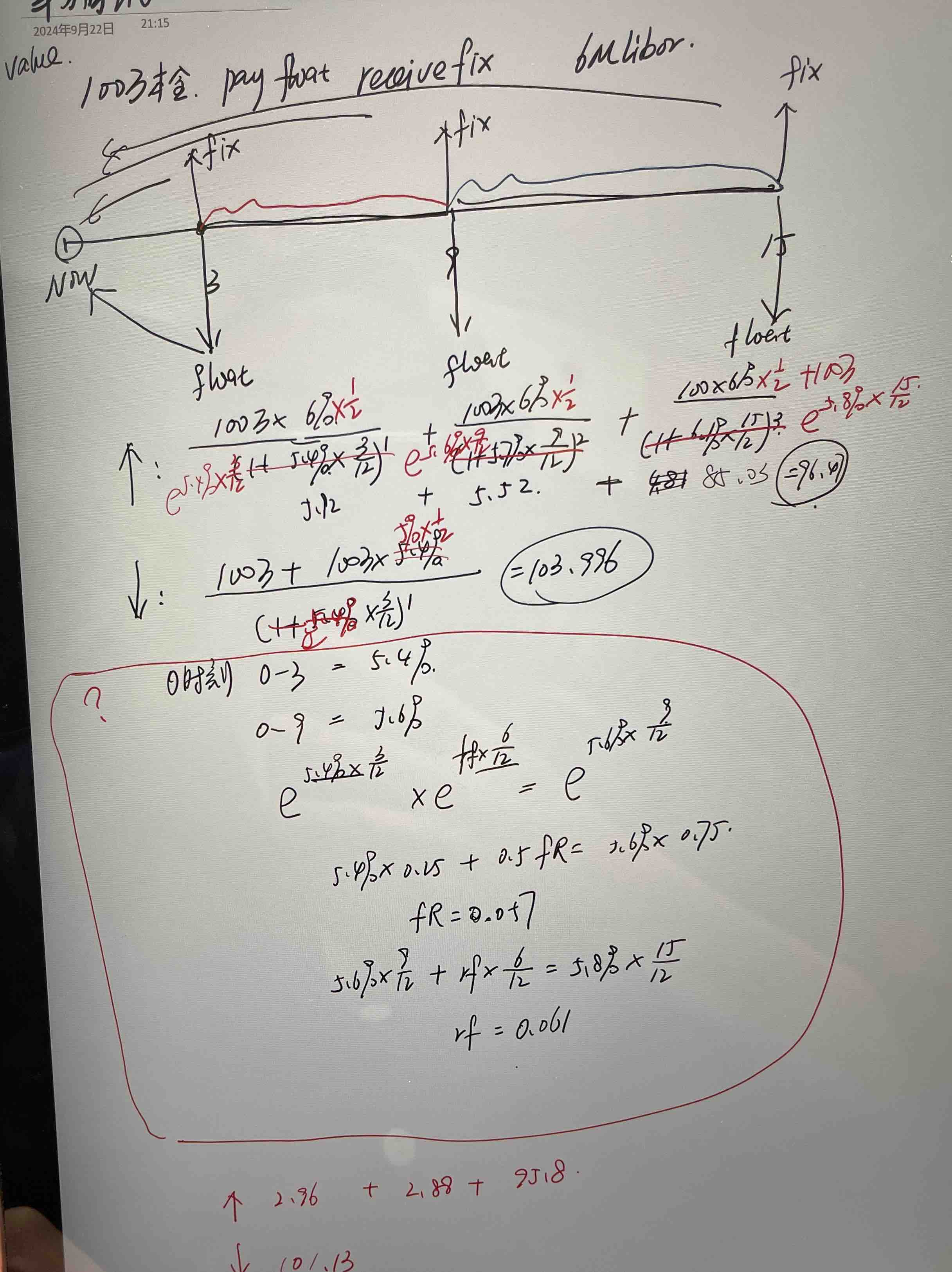

Consider a $1 million notional swap that pays a floating rate based on 6-month LIBOR and receives a 6% fixed rate semiannually. The swap has a remaining life of 15 months with pay dates at 3, 9 and 15 months. Spot LIBOR rates are as following: 3 months at 5.4%; 9 months at 5.6%; and 15 months at 5.8%. The LIBOR at the last payment date was 5.0%. Calculate the value of the swap to the fixed-rate receiver using the bond methodology.

选项:

A.

$6,077

B.

-$6,077

C.

-$5,077

D.

$5,077

解释:

老师,1、题目给的spot libor 不是即期利率吗?我理解spot libor 3个月是站在现在,3个月的利率是5.4%,9个月是站在现在5.6%,也就是0到9月,15个月就是0到15月,但是,对于float来讲,9个月的节点利率应该是第3个月决定的,也就是应该是站在现在,3到9的远期利率啊,15个月的利率应该是在第9个月决定的,也就是站在现在,9到15的远期利率。我想的哪儿错了吗?

2、考试时,给的是libor也会明确说明折现方式吗?还是给的是libor就是用单利折现?