NO.PZ2023061903000022

问题如下:

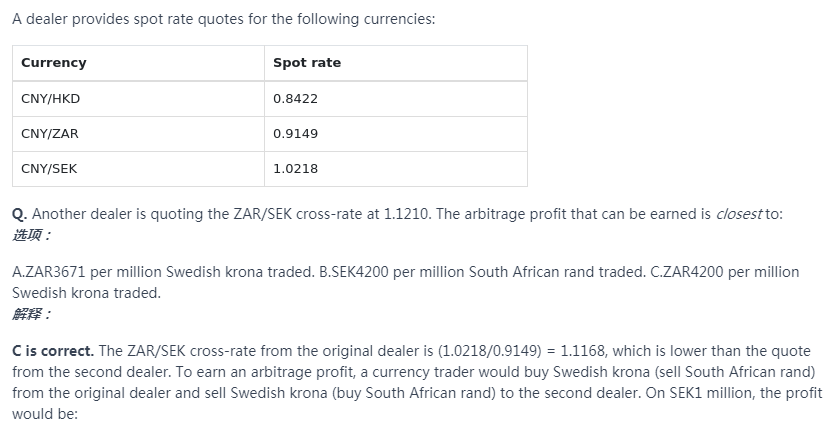

Another dealer is quoting the ZAR/SEK cross-rate at 1.1210. The arbitrage profit that can be earned is closest to:

选项:

A.ZAR3671 per million Swedish krona traded. B.SEK4200 per million South African rand traded. C.ZAR4200 per million Swedish krona traded.解释:

C is correct. The ZAR/SEK cross-rate from the original dealer is (1.0218/0.9149) = 1.1168, which is lower than the quote from the second dealer. To earn an arbitrage profit, a currency trader would buy Swedish krona (sell South African rand) from the original dealer and sell Swedish krona (buy South African rand) to the second dealer. On SEK1 million, the profit would be:

SEK1,000,000 × (1.1210 – 1.1168) = ZAR4,200

C正确。初始交易商的ZAR/SEK交叉汇率为(1.0218/0.9149)= 1.1168,低于第二家交易商的报价。为了赚取套利利润,货币交易者会从最初的交易商那里买入瑞典克朗(卖出南非兰特),然后将瑞典克朗(买入南非兰特)卖给第二个交易商。以1亿瑞典克朗计算,其利润为:

SEK1,000,000 × (1.1210 – 1.1168) = ZAR4,200

这道题目我是从“another dealer"开始显示题干的,完整的题目请告知。谢谢!