NO.PZ2023091802000126

问题如下:

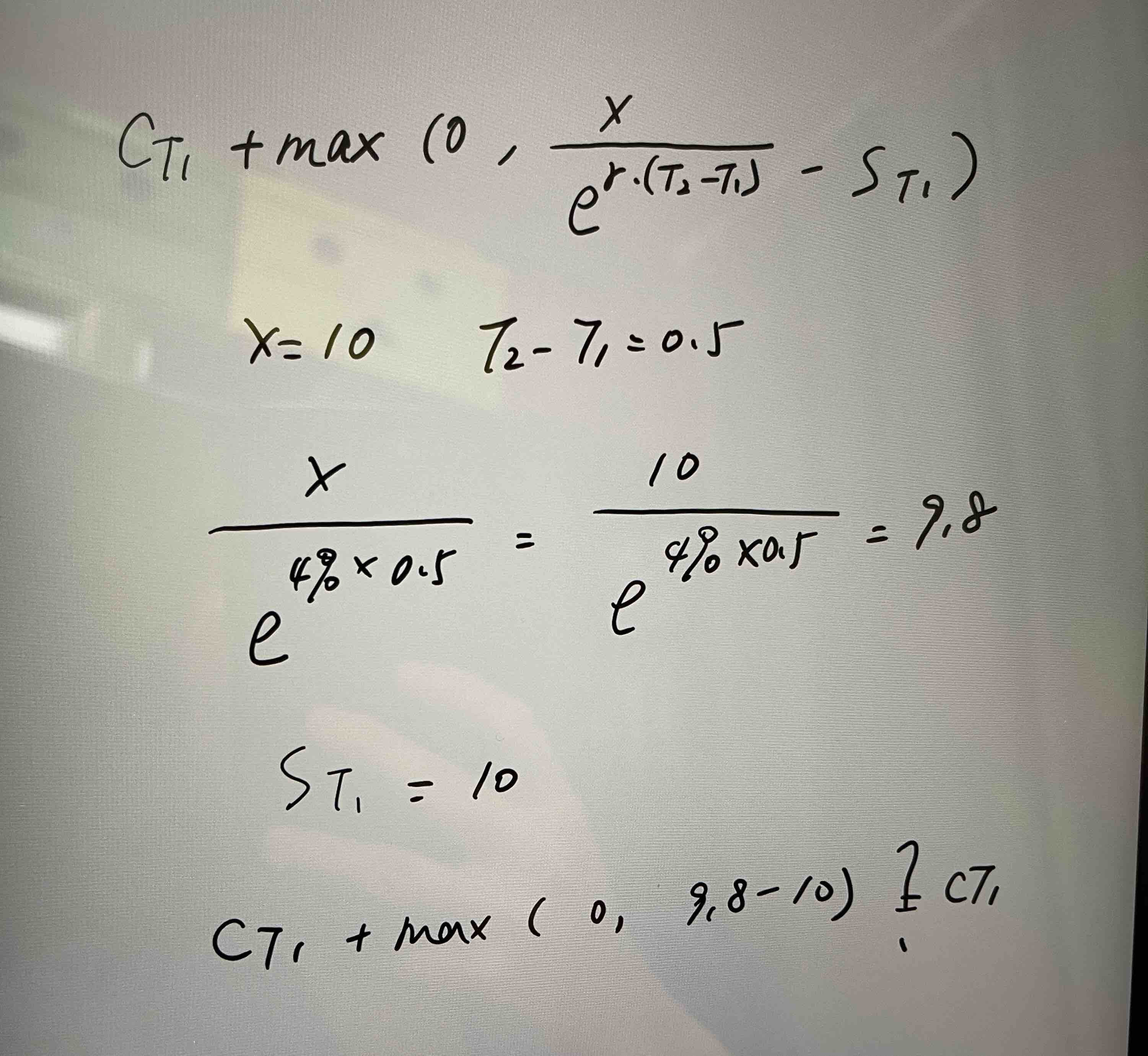

Assume a European chooser option where stock price is $10, strike price is $10, volatility is 20%, dividend yield is 0%, and risk-free rate is 4%. The choice can be made within the next six months (T1 = 0.5 year) and the option will expire in one year (T2 = 1.0 year). What is a synthetic (portfolio) equivalent to the chooser option?

选项:

A.

A call option with strike price 10 and maturity 1 year and a put option with strike price 9.80 and maturity 0.5 year.

B.

A call option with strike price 10 and maturity 0.5 year and a put option with strike price 9.80 and maturity 1 year.

C.

A put option with strike price 10 and maturity 1 year and a put option with strike price 9.80 and maturity 0.5 year.

D.

A put option with strike price 10 and maturity 0.5 year and a call option with strike price 9.80 and maturity 1 year.

解释:

老师好,不应该是一直持有一个看涨期权,没有看跌吗,因为max(0,-0.2)应该是0,还是我哪里算错了吗?