NO.PZ2023081403000095

问题如下:

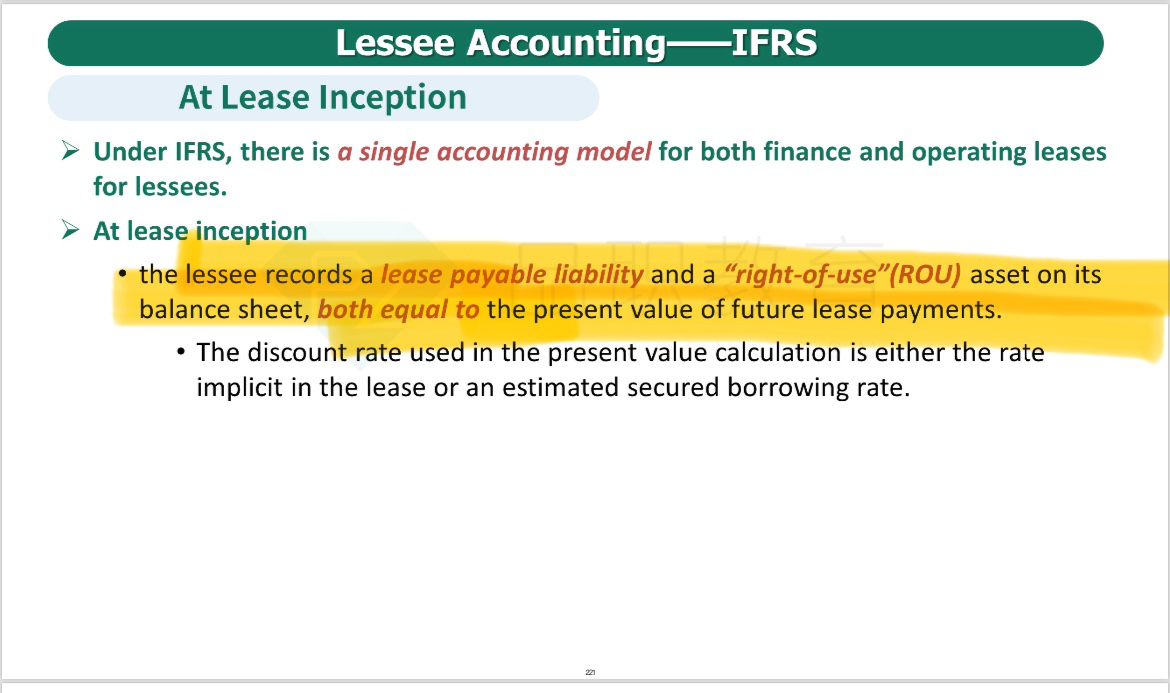

Q. A company enters into a finance lease agreement to acquire the use of an asset for three years with lease payments of EUR19,000,000 starting next year. The leased asset has a fair market value of EUR49,000,000 and the present value of the lease payments is EUR47,250,188. Based on this information, the value of the lease liability reported on the company’s balance sheet at lease inception is closest to:

选项:

A.EUR47,250,188.

B.EUR49,000,000.

C.EUR57,000,000.

解释:

A is correct. Under the revised reporting standards under IFRS and US GAAP, a lessee must recognize an asset and a lease liability at inception of each of its leases (with an exception for short-term leases). The lessee reports a right-of-use (ROU) asset and a lease liability, calculated essentially as the present value of fixed lease payments, on its balance sheet. Thus, at lease inception, the company will record a lease liability on the balance sheet of EUR47,250,188.

麻烦解释一下 谢谢~~~~