NO.PZ2024030508000050

问题如下:

A risk analyst at a high-yield bond fund is calculating the conditional probability of default (PD) for a CCC-rated bond. The analyst has the following cumulative PD data from a rating agency:

What is the conditional probability that the bond defaults during year 3?

选项:

A.5.35% B.8.17% C.19.90% D.26.10%解释:

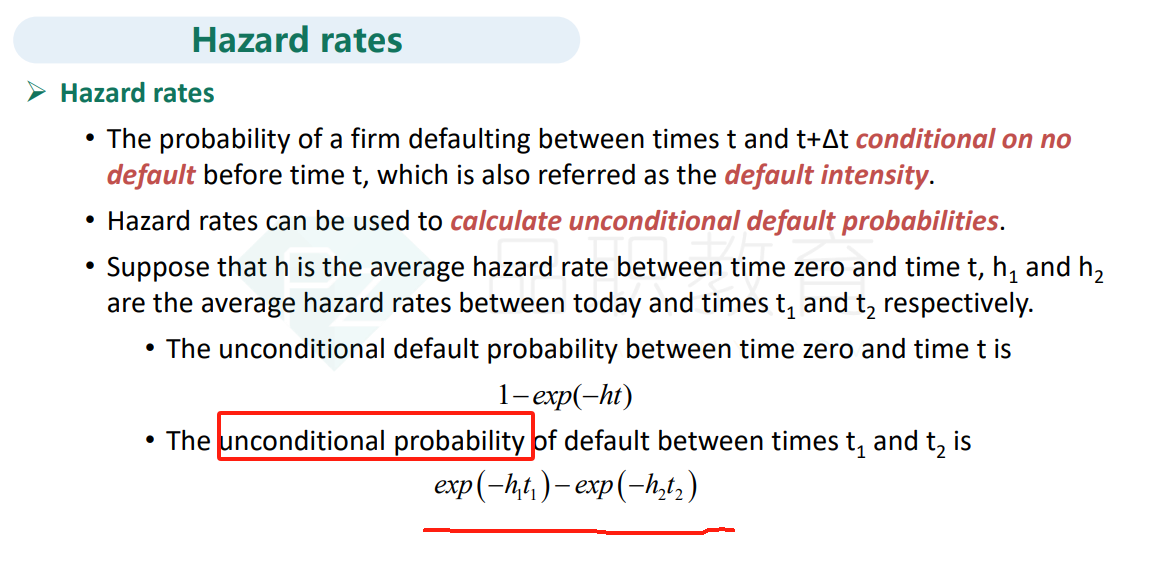

Explanation: B is correct. To calculate conditional PD in year 3, one must first calculate the unconditional PD in year 3. This equals the difference between the cumulative PDs in year 3 and year 2: 39.86% – 34.51% = 5.35%.

Conditional PD in year 3 is the PD in year 3 on the condition that the bond survives to year 3, or the unconditional PD divided by the survival rate. The survival rate to year 3 is one minus the cumulative PD to year 2: 100% – 34.51% = 65.49%. Conditional PD in year 3 is therefore 5.35% / 65.49% = 8.17%.

A is incorrect. This is the year 3 unconditional PD.

C is incorrect. This plugs the year 2 and year 3 cumulative PDs into the formula for calculating the year 3 unconditional PD from hazard rates:

= exp(−34.51% ∗ 2) − exp(−39.86% ∗ 3) = 19.90%

D is incorrect. This multiplies the survival rate to year 3 by the year 3 cumulative probability.

Learning Objective: Define conditional and unconditional default probabilities and explain the distinction between the two.

Reference: Global Association of Risk Professionals, Valuation and Risk Models (New York, NY: Pearson, 2023). Chapter 4. External and Internal Credit Ratings [VRM–4]

什么时候用答案这个公式,什么时候用e^-h*t这个公式,这个两个有什么区别?