NO.PZ2023100905000007

问题如下:

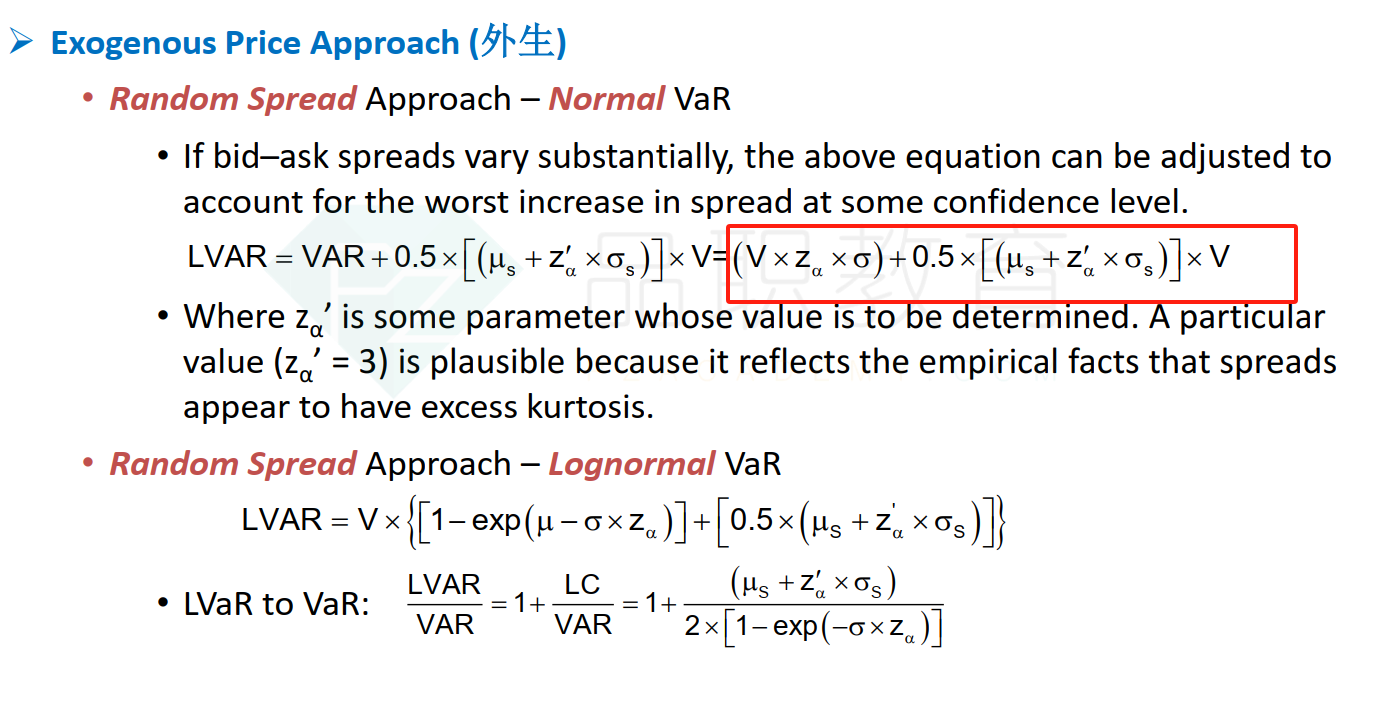

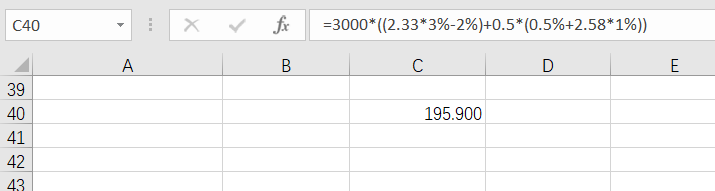

You are holding 100 SkyTrek Company shares with a current price of $30. The daily mean and volatility of the stock return are 2% and 3%, respectively. VaR should be measured relative to initial wealth. The bid-ask spread of the stock varies over time, and the daily mean and volatility of this spread are 0.5% and 1%, reactively. The return is normally distributed. What is the daily liquidity-adjusted VaR (LVaR) at a 99% confidence level assuming the confidence parameter of the spread is equal to 2.58?

选项:

A.$193.15

B.$172.62

C.$103.50

D.$195.90

解释:

麻烦提供下公式和解析带数字