NO.PZ202204250100001504

问题如下:

Which of West’s statements regarding rebalancing ranges is least likely correct?

选项:

A.Statement 1.

Statement 2.

解释:

Correct Answer: C

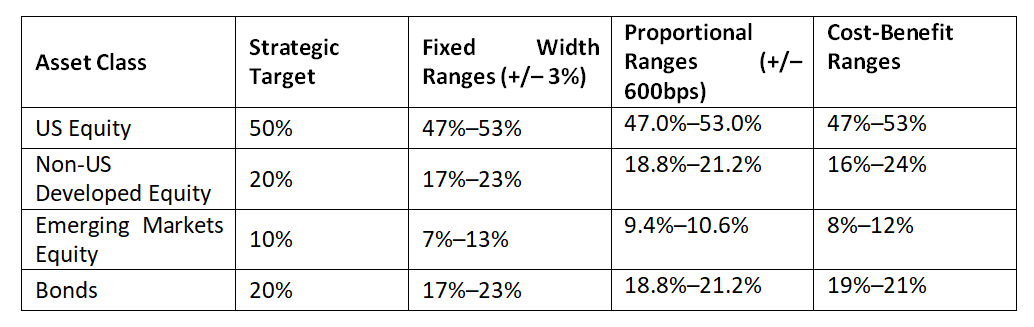

Statement 3 is incorrect. Rebalancing ranges for non-US

developed equity should be wider than US equity under the cost-benefit (not

proportional range) because it has higher transaction costs. Rebalancing ranges

under the proportional range approach are defined as +/– 600 basis points for

all asset classes in this example and are computed as follows.

Rebalancing ranges

for bonds under the proportional range approach:

20% × (1 + 600

bps) = 20% × 1.06 = 21.2%

20% × (1 – 600

bps) = 20% × 0.94 = 18.8%

Hypothetical

Rebalancing Ranges under Three Different Approaches

1.statement 3 错误的原因是因为wider是基于成本(答案中)的考虑,而不是基于风险(题干中)的考虑么,2.那为什么不能基于风险的考虑呢?