NO.PZ202305230100005305

问题如下:

The bond portfolio’s benchmark is a fixed-income index with a duration of 9.5325 and convexity of 103.0677. Based on the weighted-average portfolio duration and convexity, the portfolio should outperform its benchmark in which of the following scenarios?

选项:

A.Only when interest rates are rising

Only when interest rates are falling

Both when interest rates are rising and falling

解释:

C is correct. The portfolio has a weighted-average duration of 9.5325, which is identical to the benchmark’s duration. However, the portfolio has higher convexity (116.7493) compared to the benchmark (103.0677). All else equal, the portfolio should outperform the lower-duration benchmark portfolio in both rising and falling interest rate environments.

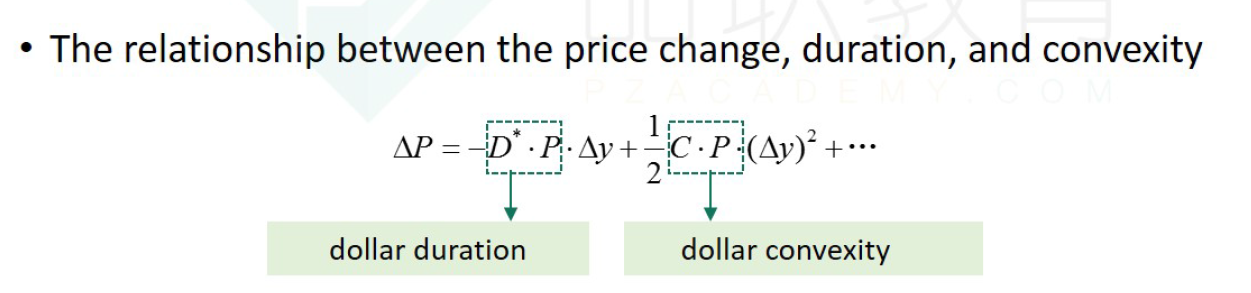

为何凸性越大组合表现越好,在相同久期情况下