NO.PZ2020012001000033

问题如下:

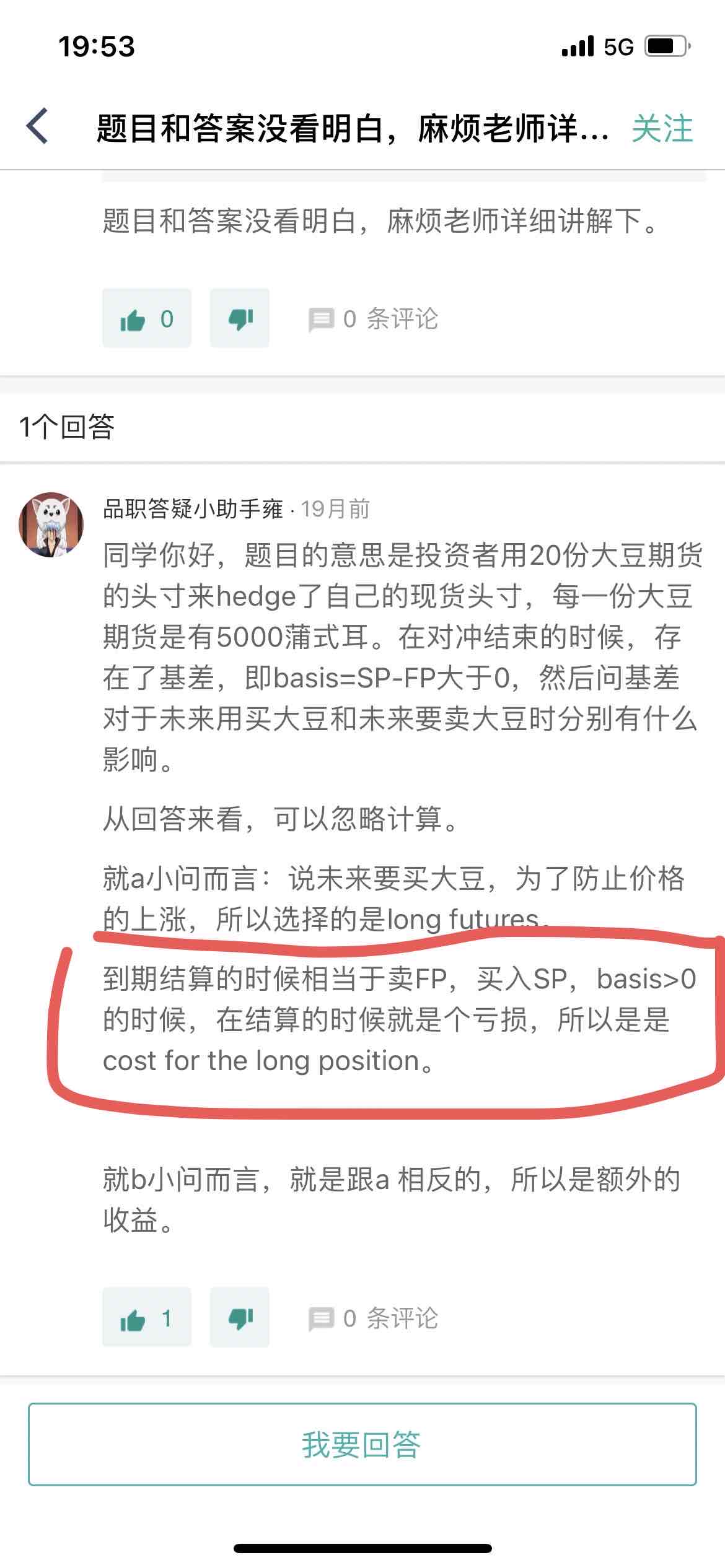

20 futures contracts are used to hedge an exposure to the price of soybeans. Each futures contract is on 5,000 bushels. At the time the hedge is closed out, the basis is 20 cents per bushel. What is the effect of the basis on the hedger if (a) the purchase of soybeans is being hedged and (b) the sale of soybeans is being hedged?

解释:

The basis increases the net price after hedging by 20 * 5,000 * USD 0.20 or USD 20,000. In (a) this is an extra cost to the hedger. In (b) it is an extra amount received from the sale of soybeans.

老师,我真的不太懂这个逻辑,就是我未来要买大豆,担心价格上涨,好……我long一个期货,这里我知道,然后说basis risk是20,正数,所以是我的现货价格涨幅要快过期货涨幅,那我应该是对冲风险对了呀,为什么我反而增加了成本??我总觉得我哪里的逻辑不对