NO.PZ2016071602000001

问题如下:

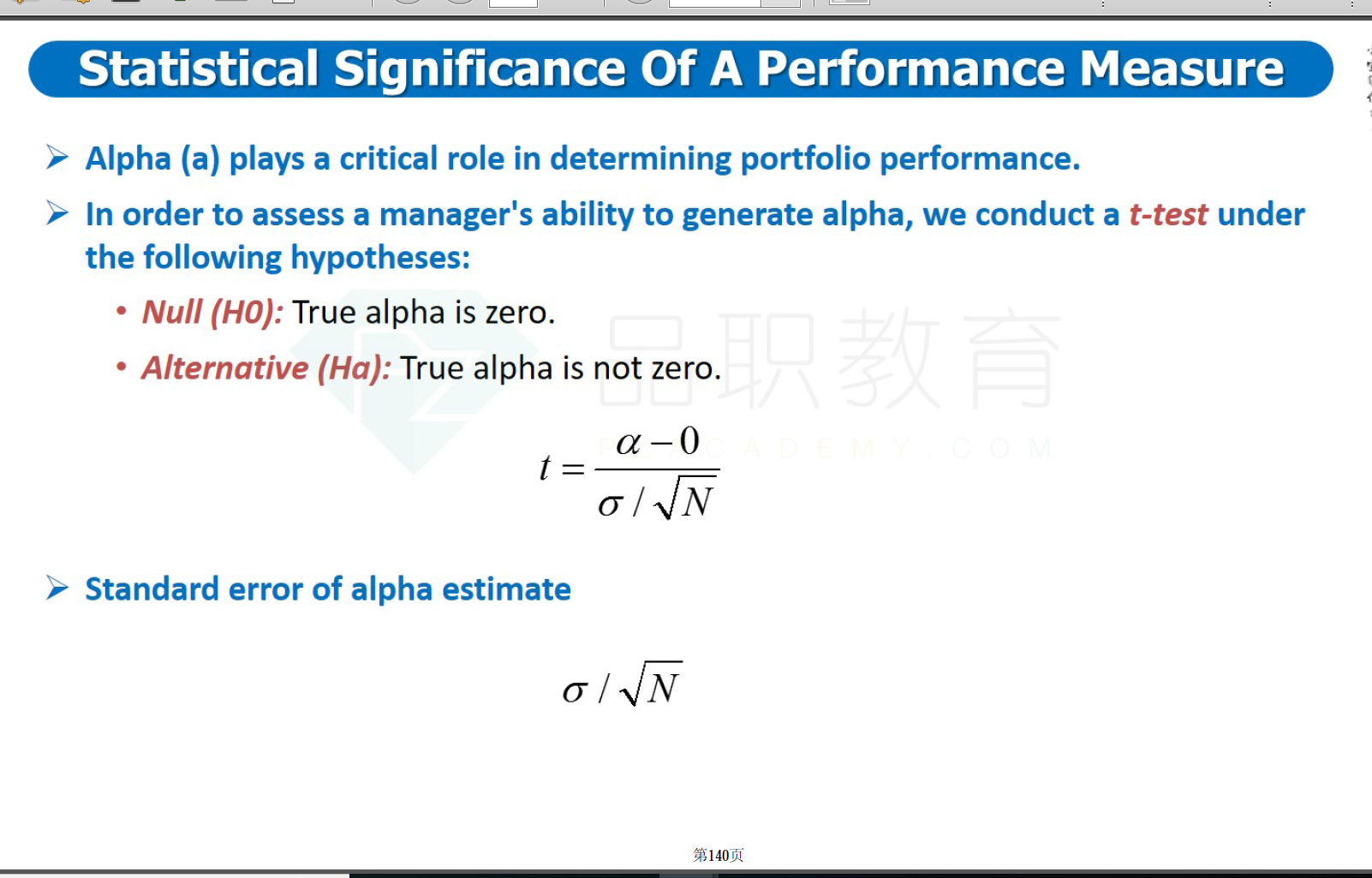

Over the past year, the HIR Fund had a return of 7.8%, while its benchmark, the S&P 500 index, had a return of 7.2%. Over this period, the fund's volatility was 11.3%, while the S&P index's volatility was 10.7% and the fund's TEV was 1.25%. Assume a risk-free rate of 3%. What is the information ratio for the HIR Fund and for how many years must this performance persist to be statistically significant at a 95% confidence level?

选项:

A.

0.480 and approximately 16.7 years

B.

0.425 and approximately 21.3 years

C.

3.840 and approximately 0.2 years

D.

1.200 and approximately 1.9 years

解释:

A is correct. The information ratio is (7.8 — 7.2)/1.25 = 0.48. Statistical significance is achieved when the t-statistic is above the usual value of 1.96. By Equation (29.5), the minimum number of years T for statistical significance is (1.96/IR)2 = 16.7. Note, however, that there is no need to perform the second computation because there is only one correct answer for the IR question.

老师, 想问一下 为什么 statistical 有时用 1。96 有时候 1。645 ? 是默认 statistical significance 就是 双尾吗 ?