NO.PZ202306130100003307

问题如下:

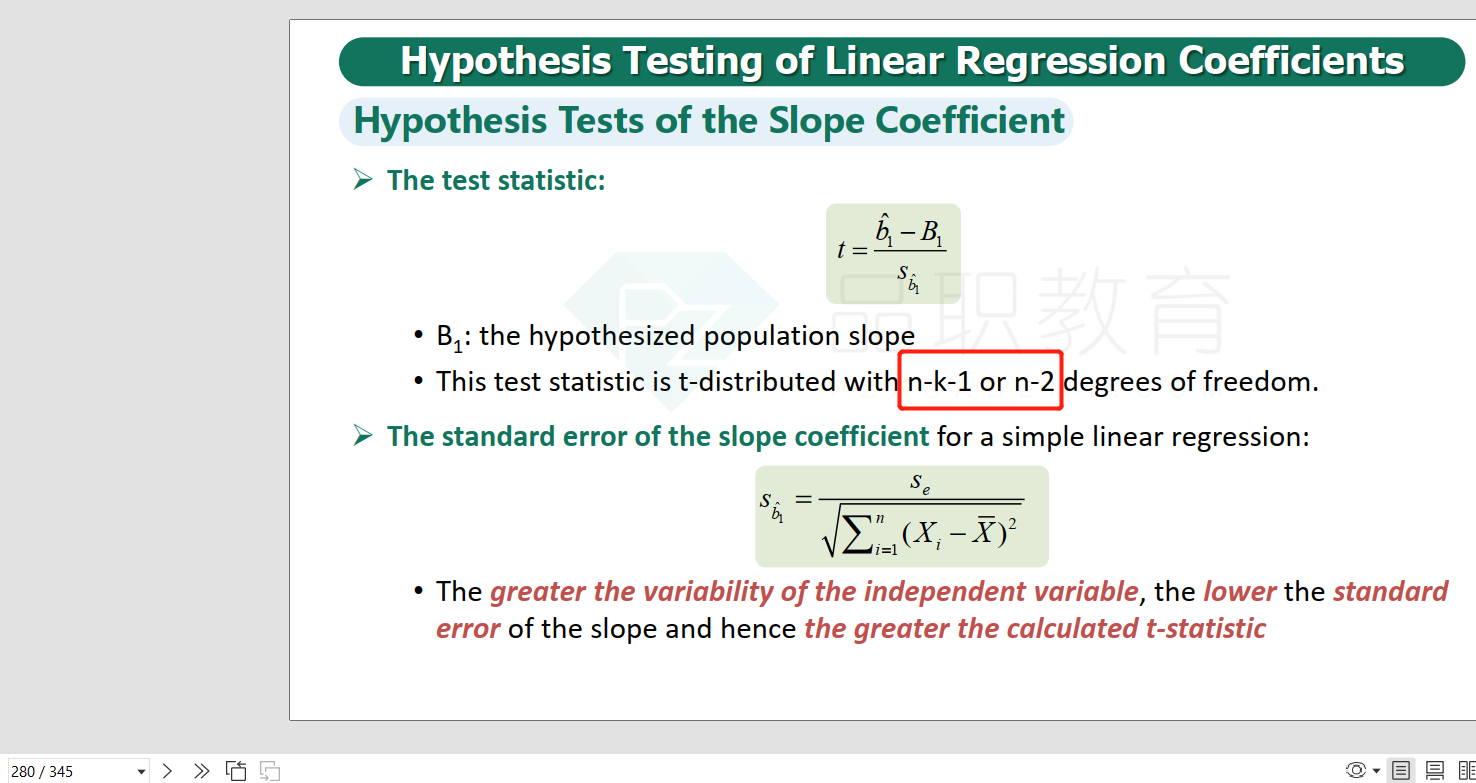

Which of the following should Liu conclude from the results shown in Exhibit 2?

选项:

A.

The average short interest ratio is 5.4975.

B.

The estimated slope coefficient is different from zero at the 0.05 level of

significance.

C.

The debt ratio explains 30.54 percent of the variation in the short interest

ratio.

解释:

B is correct. The t-statistic is −2.2219, which is outside the bounds created by the critical t-values of ±2.011 for a two-tailed test with a 5 percent significance level. The value of 2.011 is the critical t-value for the 5 percent level of significance (2.5 percent in one tail) for 48 degrees of freedom. A is incorrect because the mean of the short interest ratio is 192.3 ÷ 50 = 3.846. C is incorrect because the debt ratio explains 9.33 percent of the variation of the short interest ratio.

Short interest ratio 的自由度为何不减去1?