NO.PZ2023100703000068

问题如下:

A fund manager makes a series of strategies about volatility. Which of the following strategies is effective?选项:

A.To short volatility,he buys OTM call option.

B.When the market faces a sharp decline, he sells OTM put option.

C.When the market faces a sharp decline, he enters a variance swap as fixed variance payer.

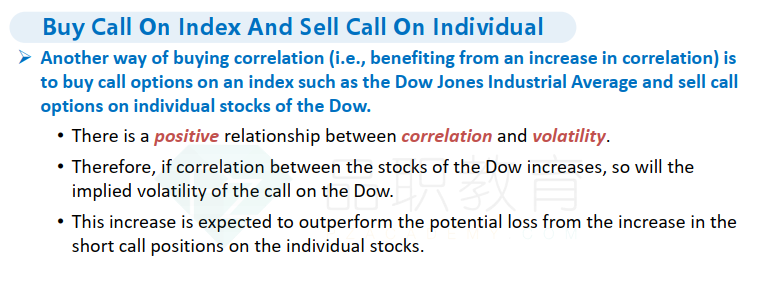

D.When correlation increase, he sells call options on an index and buys call options on individual stocks.

解释:

A is incorrect. To short volatility, he should short options, no matter they are call options or put options. B is incorrect. When the market faces a sharp decline, he should buy OTM put option.C is correct. When the market faces a sharp decline, the correlation increase, variance swap payer will benefit.D is incorrect. When correlation increase, he should buy call options on an index and sell call options on individual stocks.解释一下D,分不清如何判断buy/sell index/individual的情况