NO.PZ2023091701000092

问题如下:

An at-the-money European call option on the DJ EURO STOXX 50 index with a strike of 2200 and maturing in 1 year is trading at EUR 350, where contract value is determined by EUR 10 per index point. The risk-free rate is 3% per year, and the daily volatility of the index is 2.05%. If we assume that the expected return on the DJ EURO STOXX 50 is 0%, the 99% 1-day VaR of a short position on a single call option calculated using the delta-normal approach is closest to:

选项:

A.EUR 8

B.EUR 53

C.EUR 84

D.EUR 525

解释:

Since the option is at-the-money, the delta is close to 0.5. Therefore a 1 point change in the index would translate to approximately 0.5 × EUR 10 = EUR 5 change in the call value. Therefore, the percent delta, also known as the local delta, defined as %D = (5/350) / (1/2200) = 31.4.

So the 99% VaR of the call option = %D × VaR(99% of index) = %D × call price × alpha (99%) × 1-day volatility = 31.4 × EUR 350 × 2.33 × 2.05% = EUR 525. The term alpha (99%) denotes the 99th percentile of a standard normal distribution, which equals 2.33.

There is a second way to compute the VaR. If we just use a conversion factor of EUR 10 on the index, then we can use the standard delta, instead of the percent delta:

VaR(99% of Call) = D × index price × conversion × alpha (99%) × 1-day volatility = 0.5 × 2200 × 10 × 2.33 × 2.05% = EUR 525, with some slight difference in rounding.

Both methods yield the same result.

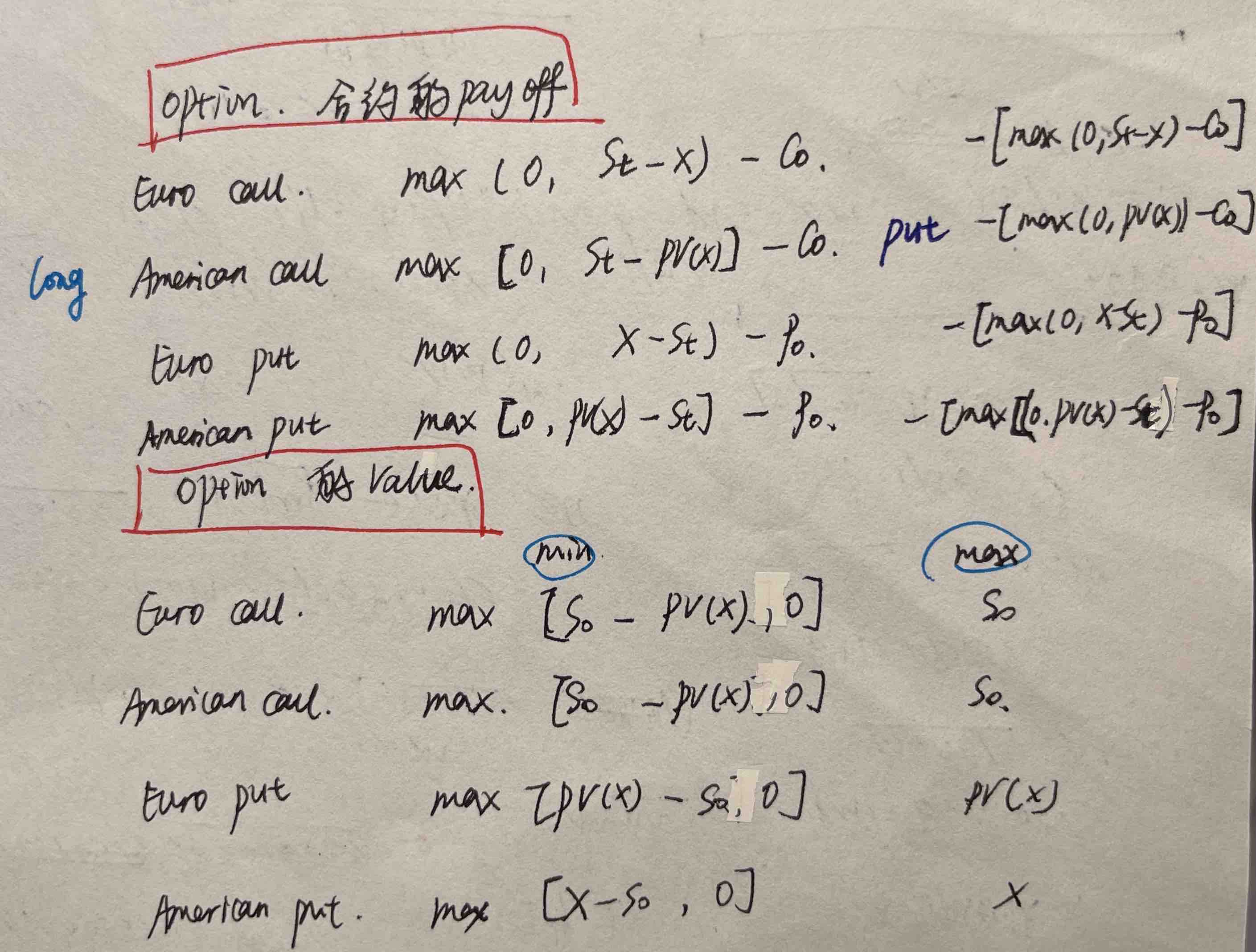

老师,1、现在是at the money ,也就是option long的一方以执行价格买股票是赚钱的对吧?

2、这里的option价格指的是option合约的价格还是option value?

3、如果是option value,指的是min还是max?不管哪个,为什么是执行价格?

4、题目只要没说明都默认欧式期权?