NO.PZ2023091701000179

问题如下:

A financial analyst at a large investment firm is evaluating and selecting MBS pools to invest in. The analyst uses a Monte Carlo simulation to value the MBS pools and to determine the option-adjusted spread (OAS) for each of the pools being examined. Which of the following statements regarding OAS and MBS valuation techniques is most appropriate?

选项:

A.The OAS valuation procedure involves making an initial estimate of the OAS, followed by conducting a Monte Carlo simulation using the yield on US Treasury bills as the discount rate.

B.When an MBS pool with a high OAS is identified, it should be purchased immediately to take advantage of this relatively attractive investment compared to other MBS.

C.The OAS valuation procedure involves continually changing the OAS estimate until the simulated price is the same as the market price.

D.Mortgage rates are perfectly correlated with US Treasury bond rates, and therefore OAS is calculated as the expected MBS return plus the return on US Treasury bonds.

解释:

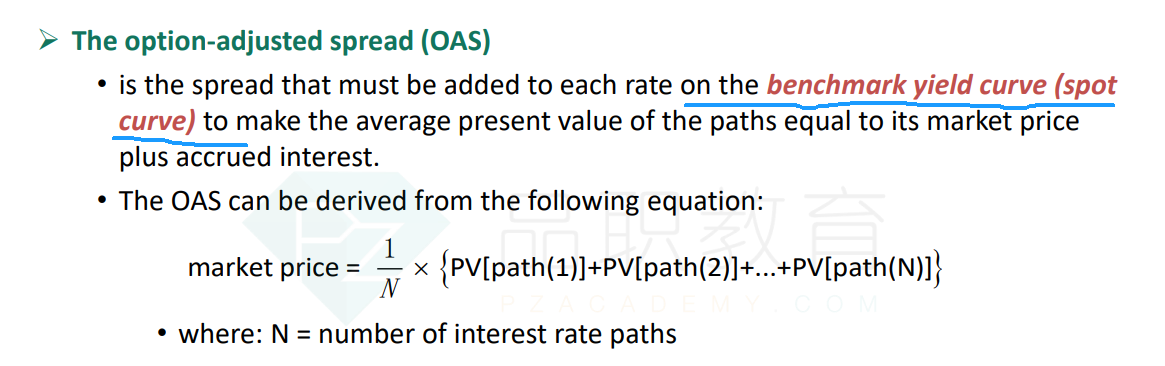

C is correct. When determining the OAS provided by the MBS, the process is:

- Make an initial OAS estimate.

- Conduct the Monte Carlo simulation using a discount rate of the Treasury rate plus the initial OAS estimate.

- Compare the result with the market price.

- If the market price is higher than the simulated one, reduce the OAS estimate, and vice-versa.

- Keep changing the OAS estimate until the simulated price is the same as the market price.

A is incorrect. When conducting the Monte Carlo simulation after making an initial estimate of the OAS, the rate used is the Treasury rate plus the initial estimate of the OAS.

B is incorrect. Rather than just immediately purchasing a high-MBS pool, the analyst should investigate technical or institutional reasons for this outlying pool. There could be an assumption in the model that needs to be examined and potentially challenged.

D is incorrect. Mortgage rates are not perfectly correlated with Treasury rates and so even if an analyst has a perfect pre-payment model that depends only on interest rates, there will always be some residual interest rate risk when Treasury instruments are used as hedges. OAS = Expected MBS Return − Return on Treasury Instruments.

老师,OAS到底是(1+spot rate+OAS)还是(1+rf+OAS)啊?课程里讲的是spot rate,经典题这题的选项都是在无风险利率(国债利率)rf的基础上加OAS