NO.PZ201602270200002005

问题如下:

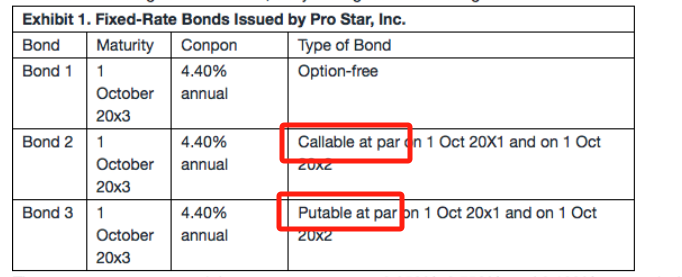

5. The value of Bond #3 is closest to:

选项:

A.102.103% of par.

B.103.688% of par.

C.103.744% of par.

解释:

C is correct.

:

-2016022702.files/image040.jpg)

S= Interest Rate Scenario

C=Cash Flow (% of par)

R=One-year Interest rate (%)

V= Value of the Callable Bond’s Future Cash Flows (% of par)

老师讲义里面说的是Value of callable高于strike price的价格只能取strike price

我理解这里的strike price是100是么?然后Putable 里面的strike price 也是100. 会有两个strike price不一样的情况么?不是很理解这后面的逻辑,麻烦老师梳理一下,谢谢!