NO.PZ2023040501000066

问题如下:

Adrienne Yu is an analyst with an international bank. She analyzes Ambleu S.A. (“Ambleu”), a multinational corporation, for a client presentation. Ambleu complies with IFRS, and its presentation currency is the Norvoltian krone (NVK).

Ambleu’s two subsidiaries, Ngcorp and Cendaró, have different functional currencies: Ngcorp uses the Bindiar franc (₣B) and Cendaró uses the Crenland guinea (CRG).

Prior to reviewing the 2016 and 2017 consolidated financial statements of Ambleu, Yu meets with her supervisor, who asks Yu the following question:

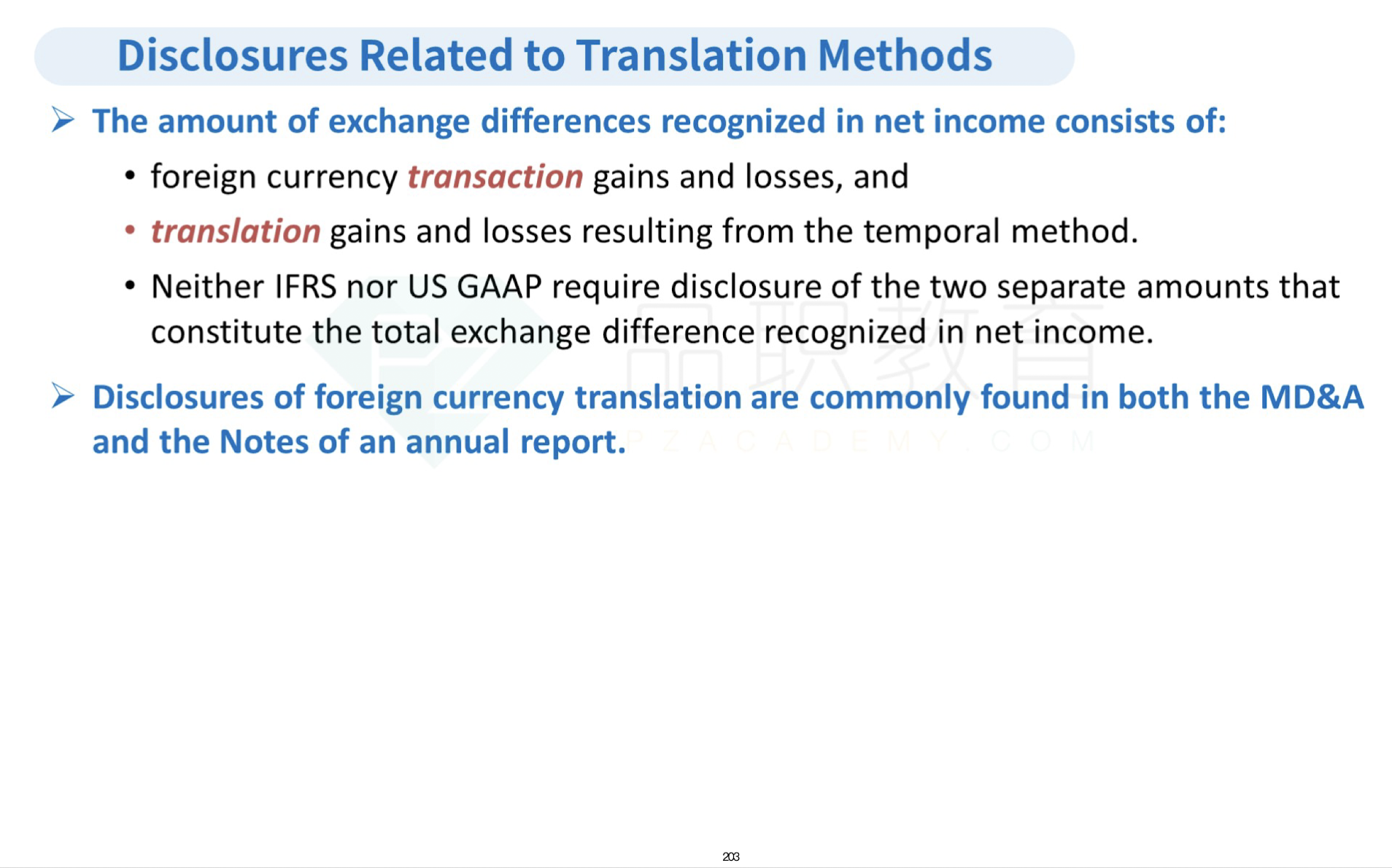

Question:According to IFRS, what disclosures should be included relating to Ambleu’s treatment of foreign currency translation for Ngcorp?

Based on Exhibit 1, the best response to Question is that Ambleu should disclose:

选项:

A.a restatement for local inflation.

that assets carried at historical cost are translated at historical rates.

the amount of foreign exchange differences included in net income.

解释:

IFRS requires that Ambleu disclose “the amount of exchange differences recognized in profit or loss” when determining net income for the period. Because companies may present foreign currency transaction gains and losses in various places on the income statement, it is useful for companies to disclose both the amount of transaction gain or loss that is included in income as well as the presentation alternative used.

老师上课讲的子公司的Functional currency不等于母公司的Reporting(Presentation) currency的时候,不是要用Current rate method吗?而且Cumulative translation adjustement(Translation Gain/Loss)计入都Equity吗?难道我理解错了?