问题如下图:

选项:

A.

B.

C.

D.

解释:

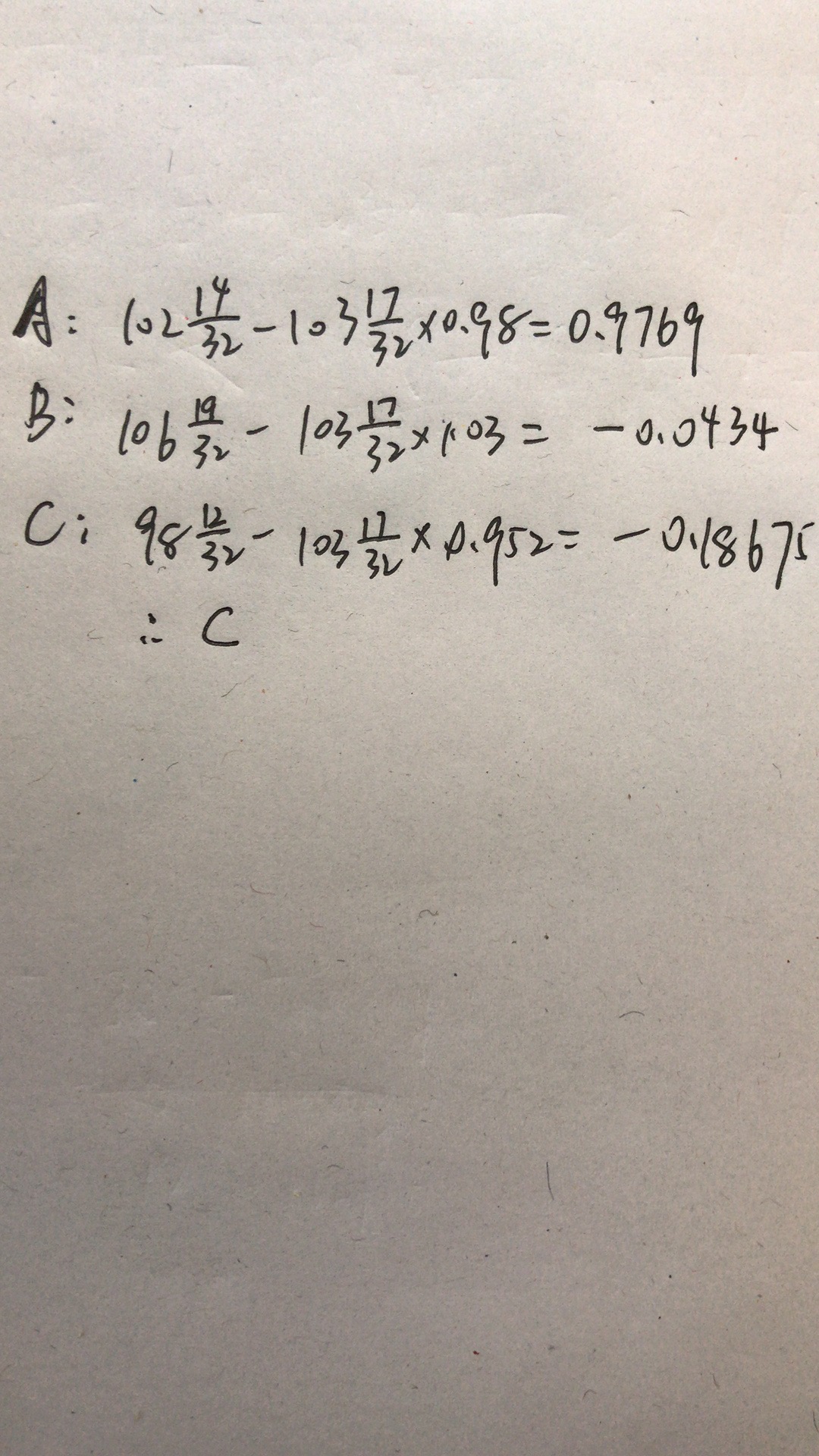

这道题按照李斯克老师视频的讲解,根据max(FP*CF-SPt)算出来最大的应该是Bond B(0.0419)才对,应该选C呀,怎么是B呀?

NO.PZ2016082402000060问题如下The yielcurve is upwarsloping. You have a short T-bonfutures position. The following bon are eligible for livery:The futures priis 103-17/32 anthe maturity te of the contrais September 1. The bon ptheir coupon semiannually on June 30 ancember 31. The cheapest to liver bonis:A.BonAB.BonCC.BonBInsufficient information ANSWER: B the complete metho minimize the cost [cost= Bonpri- Future price* conversion factor], anwe cfinchoiB(bonis the answer. CT负数表示什么

NO.PZ2016082402000060问题如下 The yielcurve is upwarsloping. You have a short T-bonfutures position. The following bon are eligible for livery:The futures priis 103-17/32 anthe maturity te of the contrais September 1. The bon ptheir coupon semiannually on June 30 ancember 31. The cheapest to liver bonis:A.BonAB.BonCC.BonBInsufficient information ANSWER: B the complete metho minimize the cost [cost= Bonpri- Future price* conversion factor], anwe cfinchoiB(bonis the answer. 想问一下这道题为啥和counpon没有关系,AI是啥

NO.PZ2016082402000060 问题如下 The yielcurve is upwarsloping. You have a short T-bonfutures position. The following bon are eligible for livery:The futures priis 103-17/32 anthe maturity te of the contrais September 1. The bon ptheir coupon semiannually on June 30 ancember 31. The cheapest to liver bonis: A.Bon B.Bon C.Bon Insufficient information ANSWER: B the complete metho minimize the cost [cost= Bonpri- Future price* conversion factor], anwe cfinchoiB(bonis the answer. 这道题目是哪个知识点,在讲义哪里?

NO.PZ2016082402000060 BonC BonB Insufficient information ANSWER: B the complete metho minimize the cost [cost= Bonpri- Future price* conversion factor], anwe cfinchoiB(bonis the answer. 用spot price减去future price乘convensionfactors

NO.PZ2016082402000060 不能直接用BonPrice/CF的方法求CT例如在No.PZ2019052801000044 中,用该方法j计算出来的结果是第三个Bon最小,实际上是第1个成本最小;