NO.PZ2023091601000078

问题如下:

Which of the

following four statements on models for estimating volatility is INCORRECT?

选项:

A.

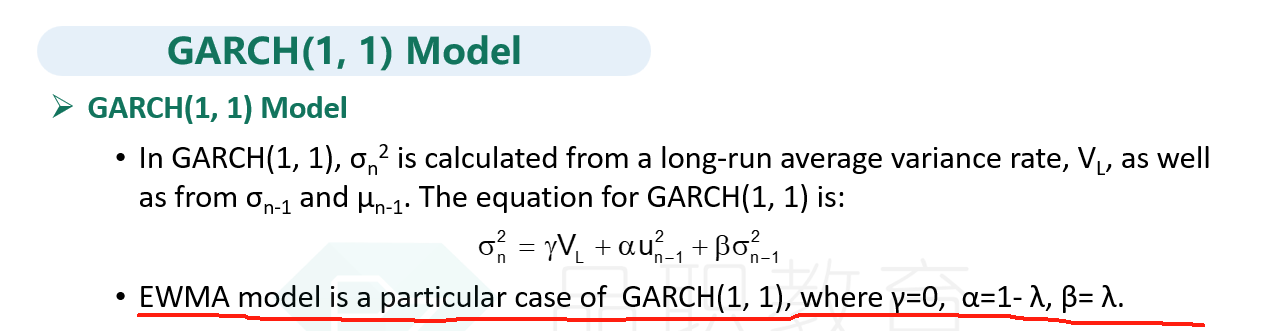

In the

exponentially weighted moving average (EWMA) model, some positive weight is

assigned to the long-run average variance.

B.

In the EWMA model,

the weights assigned to observations decrease exponentially as the observations

become older.

C.

In the GARCH (1,1)

model, a positive weight is estimated for the long-run average variance.

D.

In the GARCH (1,1)

model, the weights estimated for observations decrease exponentially as the

observations become older.

解释:

The EWMA model does

not involve the long-run average variance in updating volatility, in other

words, the weight assigned to the long-run average variance is zero. Only the

current estimate of the variance is used. The other statements are all correct.

老师好,D为什么是对的呢?GARCH哪里看出来观察值的权重呈指数减少?