NO.PZ2022062601000029

问题如下:

Jack makes the following statement regarding equity-related hedge fund managers:

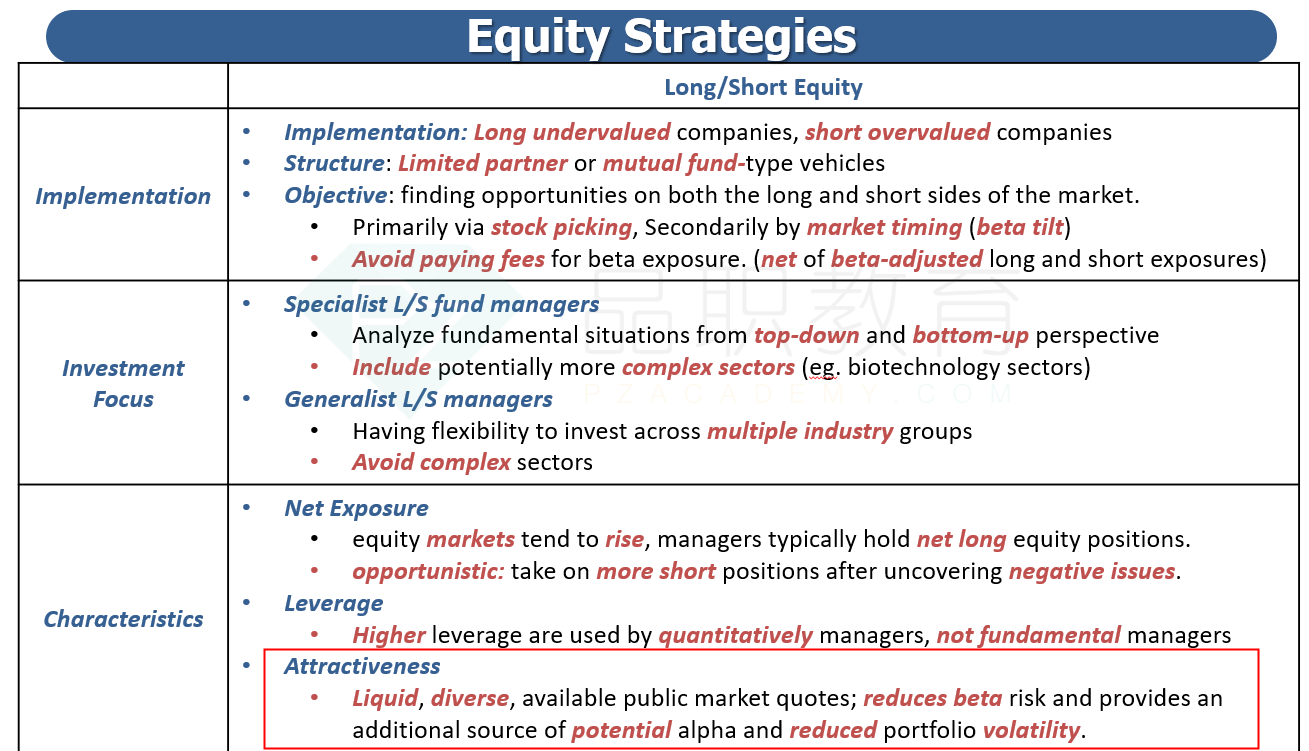

- Statement 1:The most attractive feature of long-short stock managers is that they have lower beta sensitivity to the equity market compared to long-only equity managers.

- Statement 2: Compared to long-short or equity market neutral strategies, dedicated short-bias managers typically benefit from higher levels of leverage and more frequent use of leverage.

- Statement 3: The equity market - neutral managers may have a high level of diversification and turnover.

选项:

A.Statement 1

Statement 2

Statement 3

解释:

C is correct. Jack correctly pointed out that equity market–neutral managers may have high levels of diversification and turnover.

A is incorrect. Although a lower beta to equity markets is a characteristic of long–short managers, it is not one of the attractive features of long–short strategies. If an investor wishes to have exposure to a strategy with lower equity beta, there is a cheaper way to achieve this goal by only going long.

B is incorrect. Dedicated short-bias managers typically have low levels of leverage.

知识点考察:Equity Strategies

A 不正确。long–short equity managers的特点之一是低β,但不是其相对于long-only最有有吸引的地方。因为要减少β,可以通过减少long-only得持仓来达到目的。

B 不正确。Dedicated short-bias managers通常是较低的杠杆率。毕竟做空风险高,再加杠杆会加大风险。

C 是正确的。market–neutral managers可能具有高水平的多元化和周转率。

如题