NO.PZ2024021803000027

问题如下:

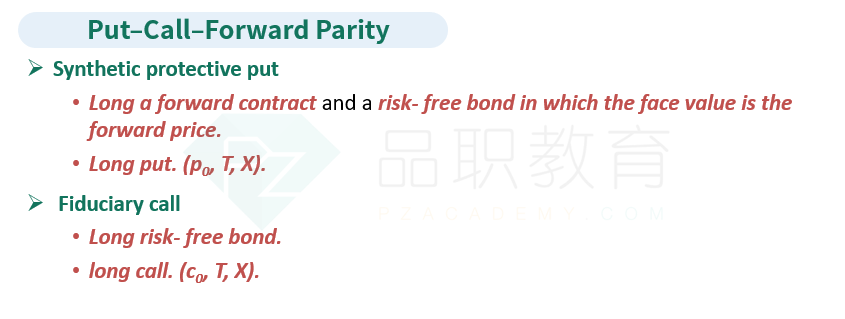

In accordance with put-call-forward parity, what is the composition of a portfolio that replicates a fiduciary call's payoff?选项:

A.A long position in a call option and a short position in a risk-free bond. B.A long position in a put option, a long forward contract, and a long position in a risk-free bond. C.A short position in a call option, a long forward contract, and a long position in a risk-free bond解释:

Put-call-forward parity explains that a fiduciary call, which is a long call combined with a risk-free bond, has the same payoff as a protective put. 根据看涨看跌远期平价,受托看涨期权(一个看涨期权和一个无风险债券的组合)与保护性看跌期权有相同的回报。不应该是short 一个零息券吗,因为等号挪过去该加负号呀