NO.PZ2023020101000011

问题如下:

They move to valuation of a bond futures

contract employed by Sheroda. Parisi provides Curry with the following

information for a Treasury bond and calculates the price of a futures contract on

this bond. The bond has a face value of $100,000, pays a 7% semiannual coupon,

and matures in 15 years. The bond is priced at $156,000, has no accrued

interest, and yields 2.5%. The futures contract expires in 8 months, and the

annualized risk-free rate is 1.5%. There are multiple deliverable bonds, and the

conversion factor for this bond is 1.098.

Based on the information provided by

Parisi, which of the following correctly calculates the futures price of the

Treasury bond:

选项:

A.f 0 ( T

)= [ $156,000 ( 1.015 ) ( 8/ 12 ) −$3,508.6958 ] /1.098 =$140,298.21.

f 0 ( T )= [ $156,000 ( 1.015 )

( 8/ 12 ) −3,491.325

]/ 1.098 =$140,314.03.

C.

f 0 ( T )=1.098[ $156,000 (

1.015 ) ( 8/ 12 ) −$3,508.6958

]=$169,144.08.

解释:

The

futures price is calculated as follows:

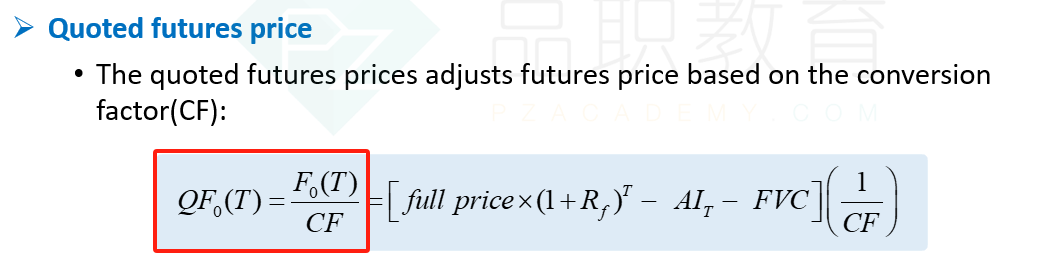

f 0 ( T )= 1 /CF( T ) { FV[ B 0 ( T+Y )+A I 0

]−A I T −FVC I 0,T }

There

is no accrued interest, but the bond pays a $3,500 coupon in 6 months, so the

future value of the coupon at expiration will be $3,508.6958 = 3500(1.015)(2/12).

f 0 ( T )= [ $156,000 ( 1.015 ) ( 8/ 12 ) −$3,508.6958 ] /1.098 =$140,298.21.

协会教材在这里写的有矛盾,参见下面两个公式,一个是需要调整AIT,但是另一个又不需要进行调整。

根据它的题目来看就是如果是根据标的资产的价格去求FP,那就不要减去AIT,但是如果要求QFP,就还需要减去AIT之后做转换.

- 老师,这道题为什么是2/12么?为什么它这个FP期权签约的时候是t=0,不是其他月份呢? 例如3月签FP,债券是半年发一次,6时发copon,11月FP到期,那就不是2/12?

- 我理解这道题求的FP,那为什么是乘以1/CF呢?