NO.PZ2023010407000016

问题如下:

Mukilteo also plans to recommend a specialist hedge fund strategy that would allow PWPF to maintain a high Sharpe ratio even during a financial crisis when equity markets fall.

The specialist

hedge fund strategy that Mukilteo plans to recommend is most likely:

选项:

A.cross-asset volatility trading between the US and

Japanese markets.

selling equity volatility and collecting the

volatility risk premium.

buying longer-dated out-of-the-money options on VIX

index futures.

解释:

C is correct.

Mukilteo needs to recommend a specialist hedge fund strategy that can help PWPF

maintain a high Sharpe ratio even in a crisis when equity markets fall. Buying

longer-dated out-of-the-money options on VIX index futures is a long equity

volatility position that works as a protective hedge, particularly in an equity

market crisis when volatility spikes and equity prices fall. A long volatility

strategy is a useful potential diversifier for long equity investments (albeit

at the cost of the option premium paid by the volatility buyer). Because equity

volatility is approximately 80% negatively correlated with equity market returns,

a long position in equity volatility can substantially reduce the portfolio’s

standard deviation, which would serve to increase its Sharpe ratio.

Longer-dated options will have more absolute exposure to volatility levels

(i.e., vega exposure) than shorter-dated options, and out-of-the-money options

will typically trade at higher implied volatility levels than at-the-money

options.

A is incorrect

because cross-asset volatility trading, a type of relative value volatility

trading, may often involve idiosyncratic, macro-oriented risks that may have

adverse effects during an equity market crisis.

B is incorrect

because the volatility seller is the provider of insurance during crises, not

the beneficiary of it. Selling volatility provides a volatility risk premium or

compensation for taking on the risk of providing insurance against crises for

holders of equities and other securities. On the short side, option premium

sellers generally extract steadier returns in normal market environments.

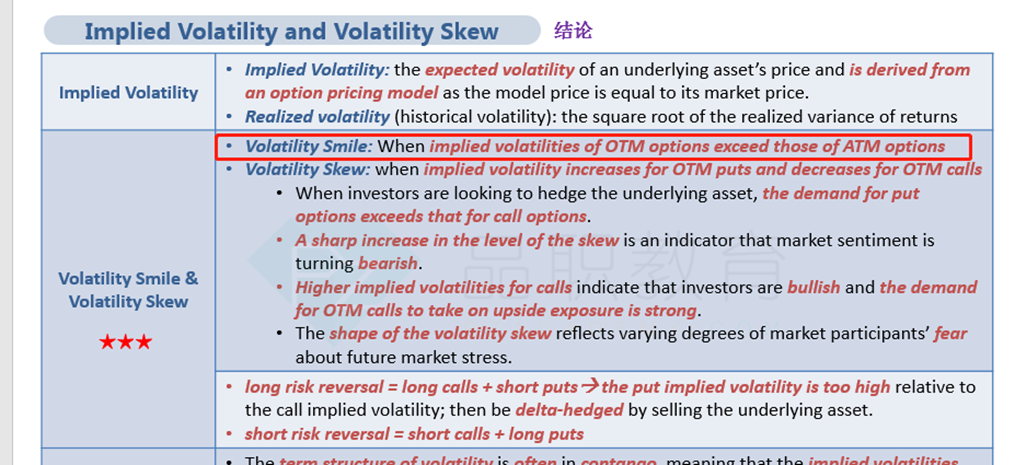

选项的解析中提到: out-of-the-money options will typically trade at higher implied volatility levels than at-the-money options.

请教一下老师这句话如何理解?