问题如下图:

选项:

A.

B.

C.

D.

解释:

这道题是考的这一章哪个kao'diao考点,没有太懂,能解释下吗?

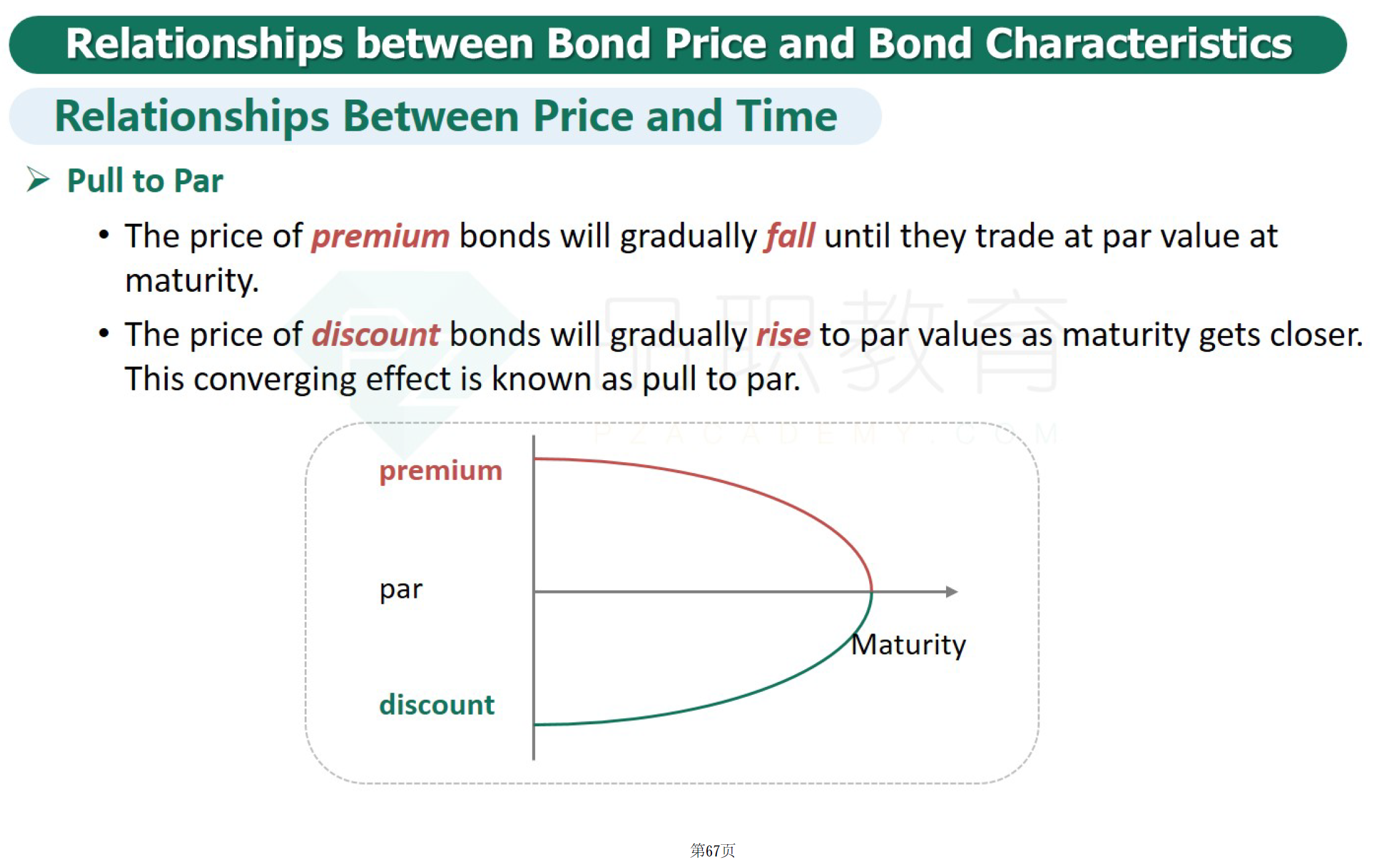

NO.PZ2016082402000004问题如下 A five-year corporate bonpaying annucoupon of 8% is sola prireflecting a yielto maturity of 6%. One yepasses anthe interest rates remain unchange Assuming a flterm structure anholng all other factors constant, the bons priring this periowill have Increased creased Remained constant Cannot terminewith the ta given ANSWER: B Because the coupon is greater ththe yiel the bonmust selling a premium or current prigreater ththe favalue. If yiel not change, the bonpriwill converge to the favalue. Given thit starts higher, it must crease. YTM为什么小于利率是溢价发行

这是哪段知识点啊?

如果是折价发行的债券,随着时间kjin靠近t时刻,价格应该也会减少吧?因为time value 减少

请问是否可以用公式计算当期price来做比较,比如p0=coupon按ytm折现,p1也按coupon折现,但是少了一个coupon,所以价格下降了?