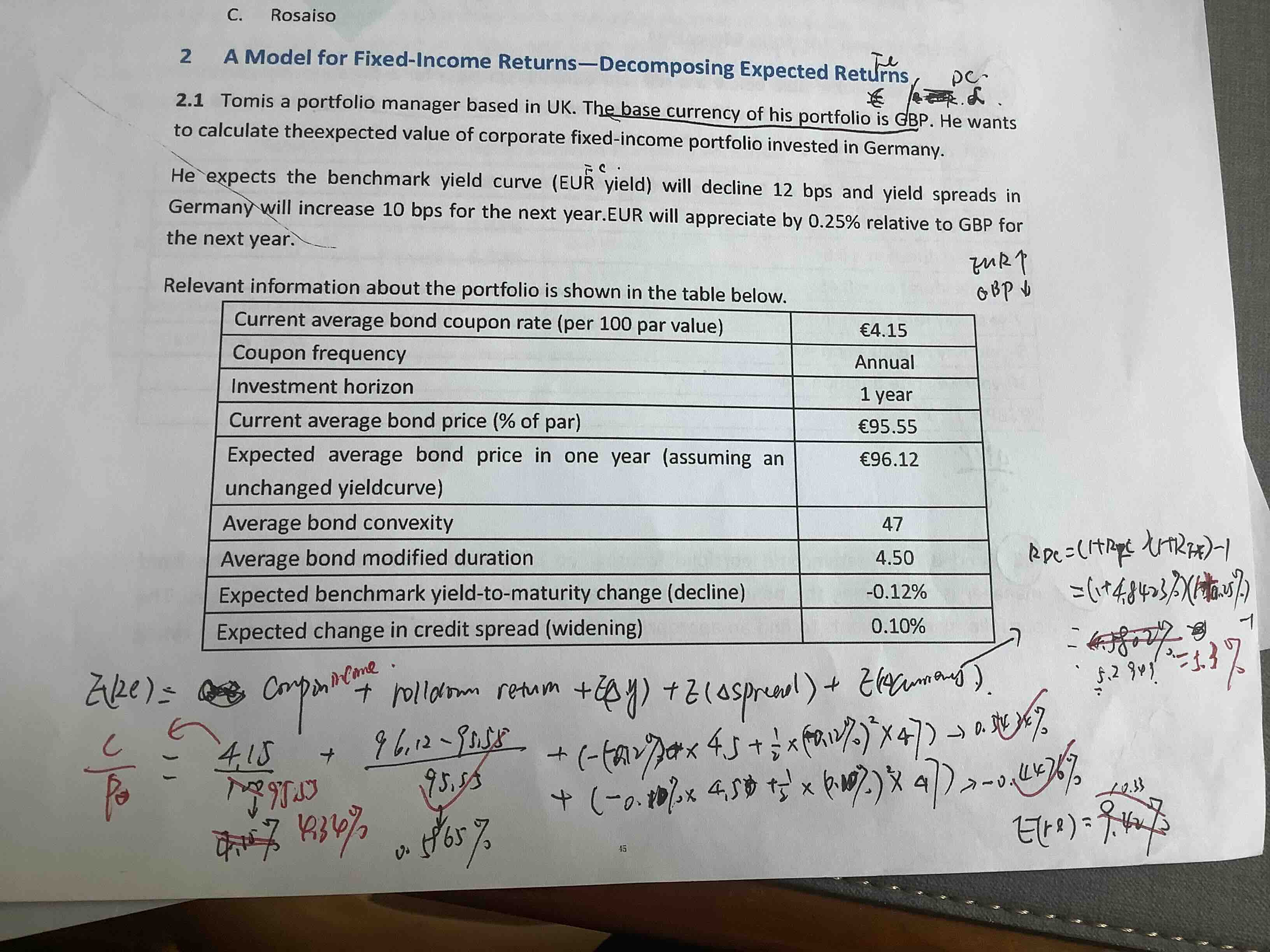

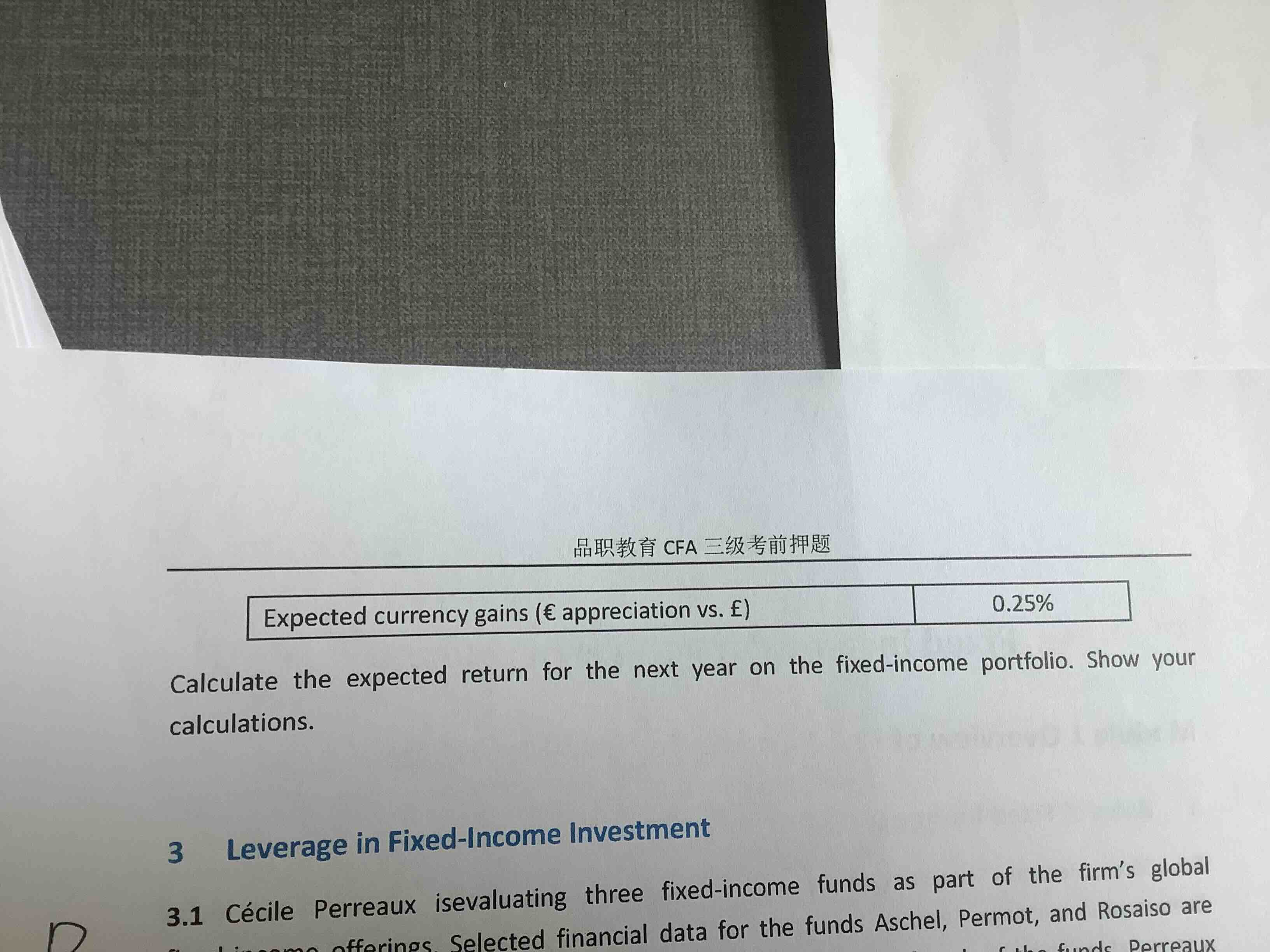

NO.PZ2018120301000004

问题如下:

After further review of the composition of each of the funds, Cécile makes the following notes:

- Note 1: Aschel is the only fund of the three that uses leverage.

- Note 2: Rosaiso is the only fund of the three that holds a significant number of bonds with embedded options.

Based on Note 2, Rosaiso is the only fund for which the expected change in price based on the investor’s views of yields to maturity and yield spreads should be calculated using:

选项:

A.

convexity

B.

modified duration.

C.

effective duration.

解释:

C is correct. Rosaiso is the only fund that holds bonds with embedded options. Effective duration should be used for bonds with embedded options. For bonds with embedded options, the duration and convexity measures used to calculate the expected change in price based on the investor’s views of yields to maturity and yield spreads are effective duration and effective convexity. For bonds without embedded options, convexity and modified duration are used in this calculation.

这道题是不是答案有点问题。它第二句说的是base currency是GBP,那么标价形式应该是EUR/GBP,然后EUR升值0.25%不是相当于GBP贬值0.25%吗,根据

R(DC)=(1+R(FC))(1+(R(FX))—1这个公式,R(FX)应该是—0.25%才对呀,答案为什么是0.25%呢