NO.PZ2023100703000102

问题如下:

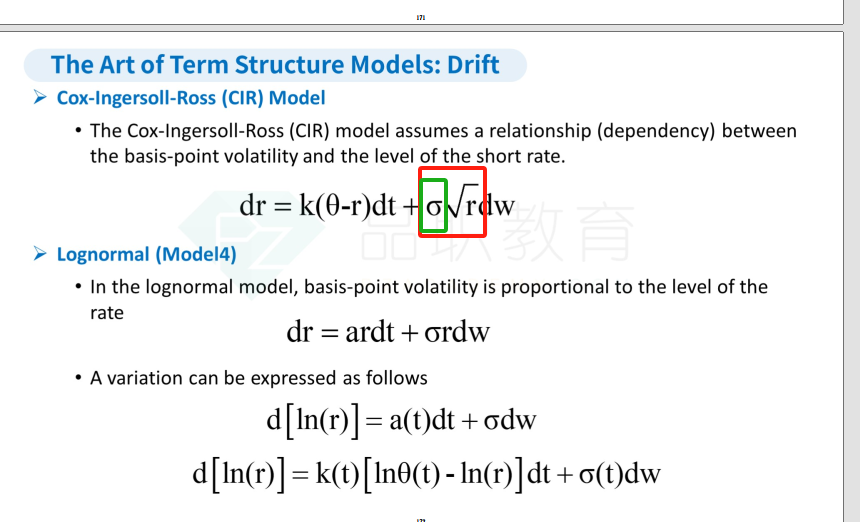

An analyst on a fixed-income desk of a large investment company is studying term structure models that incorporate measures of volatility into the interest rate process. The analyst focuses on the Cox-Ingersoll-Ross (CIR) model and its treatment of volatility of the short-term interest rate. Which of the following statements is correct regarding the yield volatility and basis-point volatility in the CIR model?

选项:

A.Periods of extremely low short-term interest rates are accompanied by high basis-point volatility, which increases the possibility of negative interest rates in the CIR model.

B.In the CIR model, basis-point volatility is specified as a decreasing function of the mean reversion factor.

C.In the CIR model, yield volatility is specified as being constant while basis-point volatility is allowed to vary.

D.Basis-point volatility and yield volatility are used interchangeably to measure the same volatility in the CIR model.

解释:

C is correct. In the CIR model, basis-point volatility is a function of the yield volatility, which is assumed to be constant and the square root of the short rate. Therefore, by assumption yield volatility is constant and basis-point volatility varies. A is incorrect. CIR states that when short-term interest rates are very low, basis point volatility will also be very low, which decreases the possibility of negative interest rates. This possibility can be removed entirely if a positive drift factor that is larger than the impact of volatility is included in the model. B is incorrect. In CIR, basis-point volatility is specified as an increasing function of the short rate. D is incorrect. Basis-point volatility and yield volatility are measured in different units, but they do not measure the same volatility in the CIR model.basis points V与yield V分别是公示第一项与第二项吗