NO.PZ2022062601000025

问题如下:

Investor John evaluated the U-fund, which is a convertible bond strategy. In order to gain a more accurate understanding of fund investment styles, John studied various trading examples used by U fund managers to generate alpha. Exhibit 1 provides data on recent transactions in which managers have been involved.

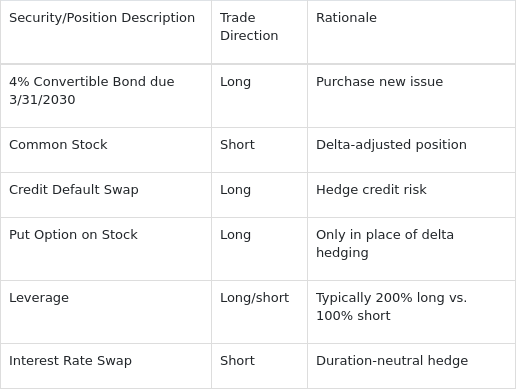

Exhibit 1

U-Fund Convertible Bond Arbitrage Position

Based on the data in Exhibit 1, what strategy is the most likely to be implemented by the portfolio manager of Fund U?

选项:

A.Taking advantage of option mispricing

Profiting from extreme market volatility

Going long a put on the equity net of hedging

解释:

A is correct. In order to obtain and extract relatively cheap embedded options in convertible securities, the manager hedged other risks embedded in convertible securities. These risks include interest rate risk, credit risk, and market risk. These risks can be hedged through a combination of interest rate derivatives, credit default swaps, and short selling the appropriate Delta adjusted amount of the underlying stock, or by purchasing put options.

B is incorrect because convertible arbitrage strategies perform best in moderate volatility. Heightened volatility would suggest a period of illiquidity and widening credit spreads.

C is incorrect because purchasing convertible bonds and Delta hedging positions do not equate to long put positions.

知识点考察:Convertible Bond Arbitrage。

首先看到表格中红框的这几项,联想到Convertible Bond Arbitrage,long CB short stock,同时使用杠杆。然后表格中剩下的没有红框的内容是是针对convertible arbitrage strategy中的convertible security的interest rate risk, credit risk of the corporate issuer, and market

risk进行对冲,相应的对冲工具也是表格中的内容interest rate derivatives, credit default swaps, and short sales of

an appropriate delta-adjusted amount of the underlying stock or, alternatively,

the purchase of put options。

所以判断是Convertible Bond Arbitrage。然后这个策略实际就是利用Convertible Bond由于新发行时交易量小,债券的复杂性导致其内嵌的option波动低,因此其交易价格低于其自身价值,也就是被低估,所以做多Convertible Bond。这正是选项A的Taking advantage of option mispricing。所以选择A。

在本题中,net neutral是否是通过 long convertible bond200%+short stock100%再加上long put option(100%)这么抵扣实现的?