NO.PZ2022123002000064

问题如下:

Hood believes that bond yields will begin an upward trend and wants

to adjust the duration of the balanced fund’s fixed income portfolio for the

next two years. Bullseye’s head trader informs Hood that he can implement this

duration adjustment using a pay-fixed, receive-floating interest rate swap.

Hood considers the

selected swap contracts shown in Exhibit 2. He knows that he can obtain the

required interest rate exposure using any one of these contracts, but his

objective is to minimize the notional principal of the swap.

Exhibit 2 Selected Pay-Fixed, Receive-Floating Swap Contracts

Determine

which counterparty’s swap contract will best achieve Hood’s objective. Justify

your response.

选项:

解释:

Correct Answer:

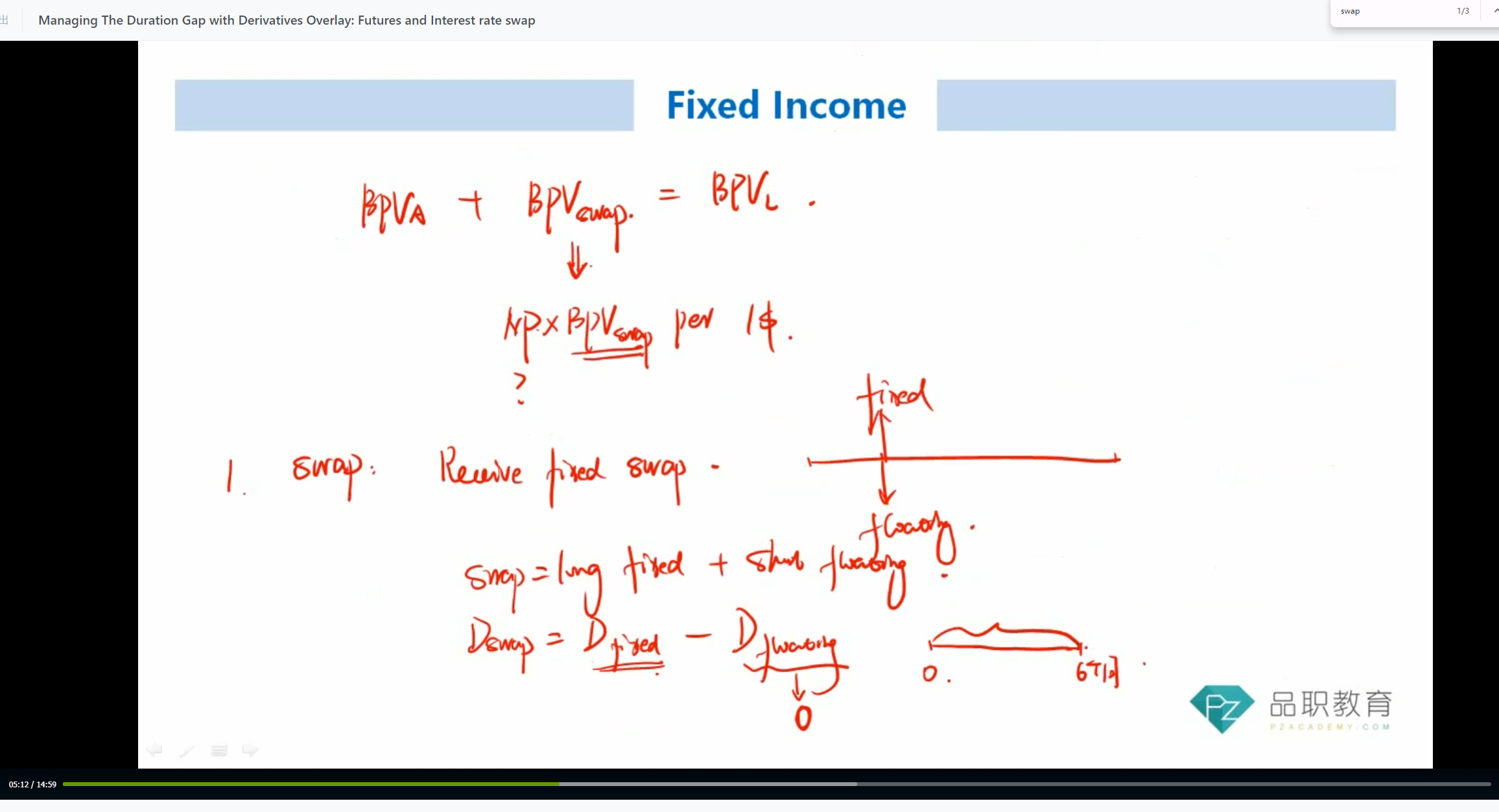

The Canis swap contract will best achieve Hood’s objective because it

is the alternative with the smallest required notional principal. The duration

of a pay-fixed, receive-floating interest rate swap is equal to the duration of

a floating-rate bond minus the duration of a fixed-rate bond, where the bonds

have cash flows equivalent to the corresponding cash flows of the swap. The

duration of the fixed leg is 75% of its maturity and the duration of the

floating leg is 50% of its payment frequency period.

The swap duration for each swap in Exhibit 2 is calculated below:

Swap duration =

Duration of floating leg – Duration of fixed leg

Duration of Orion contract (three-year maturity with quarterly

payments) = 0.125 – 2.25 = –2.125

Duration

of Ursa contract (three-year maturity with semiannual payments) = 0.25 – 2.25 =

–2.00

Duration

of Canis contract (five-year maturity with quarterly payments) = 0.125 – 3.75 =

–3.625

Duration

of Lupus contract (five-year maturity with semiannual payments) = 0.25 – 3.75 =

–3.50

In this case, because the Canis contract has the longest maturity and

the highest payment frequency, its duration is the most negative of the four

alternatives.

The notional principal of a swap (with duration MDURS) needed to change

the duration of a bond portfolio, with a market value of B, from its current

duration of MDURB to a target duration of MDURT is calculated as: NP = B x

[(MDURT – MDURB)/MDURS)

Therefore using a swap with a higher (negative) duration requires a

lower notional principal (NP) for the same-sized adjustment to portfolio

duration.

老师,答案的知识点好像有点印象,但具体查找讲义又没找到,可否麻烦老师讲解一下?谢谢!