NO.PZ2022062601000022

问题如下:

Randy and Matt are college students majoring in finance, and they discuss how to ultimately determine the foundation's evaluation process for alternative investment performance. Randy said to Matt," You measure the performance of private equity investments based on the broad stock market index, and private credit based on the investment grade fixed income index. Both targets a benchmark post tax return of over 200 basis points. These are also in line with industry practice. We will use the quarterly report values of each fund and the market value of the index to measure returns and return volatility. A difference between publicly traded and alternative asset components in portfolios is that foundations need to establish procedures to monitor alternative investment managers and processes."

Randy's comment on alternative investment evaluation to Matt is most inappropriate in the following aspects:

选项:

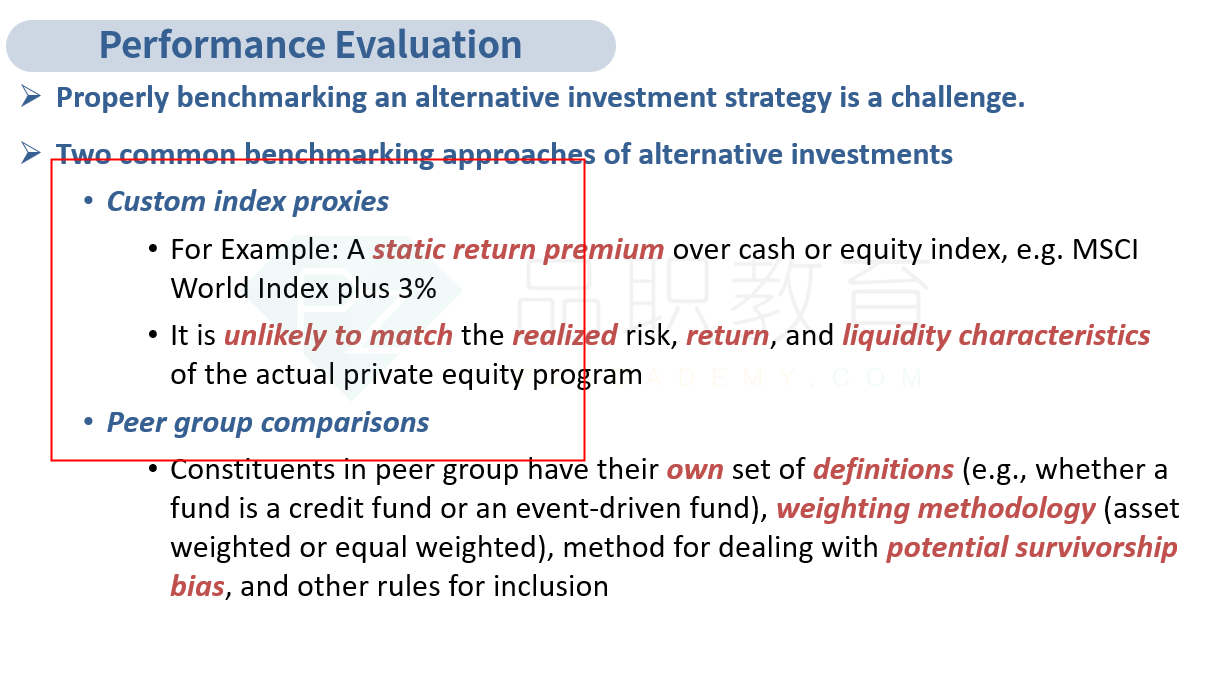

A.benchmarks for private investments.

valuation and risk of alternative investments.

the need to monitor managers and investment processes.

解释:

B is correct. Infrequent pricing (in this case, quarterly pricing) may make measuring volatility and correlation difficult because there is too little available observational data. In addition, stale pricing and the use of appraisals for valuation lead to smoothing effects (swings in market values are muted), which actually underestimates return volatility and reduces the correlation with measured returns of publicly traded assets, making the diversification benefits of alternative assets appear better than they actually are. When measuring the performance of alternative investments, efforts must be made to correct these biases.

A is incorrect. Although no benchmark for alternative investments is perfect, Randy's benchmark is in line with industry practice and is appropriate considering the nature of the investment (non venture for private equity and direct lending for private credit).

C is incorrect. For alternative investments, investors do need to pay attention to many aspects of the investment process, including key-person risks, conflicts of interest between general partners and investors, style drift, client and asset turnover, and the reliability of service providers. Investors do not need to monitor managers or investment processes when investing in publicly traded assets, as these assets are often more transparent and subject to stricter regulations.

知识点考察:Asset Allocation Approaches

B 是正确的。不频繁的定价(在这种情况下为季度定价)会使衡量波动性和相关性变得困难,因为可用的观测值太少。此外,陈旧的定价和使用评估进行估值会导致平滑效应(市场价值的波动减弱),这实际上低估了回报波动性并降低了与公开交易资产的衡量回报相关性,使得另类资产的多元化收益似乎优于他们实际情况。在衡量另类投资的表现时,必须努力纠正这些偏差。

A 不正确。尽管另类投资没有完美的基准,但 Randy 确定的基准符合行业惯例,并且考虑到投资的性质(私募股权的非风险投资和私人信贷的直接贷款)是适当的。

C 不正确。对于另类投资,投资者确实需要关注投资过程的许多方面,包括关键人物风险、普通合伙人与投资者之间的利益冲突、风格漂移、客户和资产周转率、服务提供商的可靠性等在。一般来说,投资者在投资公开交易资产时不需要监控经理或投资过程,因为这些资产往往更透明,监管更严格。

能理解b是错的,但a这里(虽是行业惯例)为什么会用IG index。。。这两个index 选择不是很明白(虽然知道不完美,但总有些优点吧?)