NO.PZ2016031001000171

问题如下:

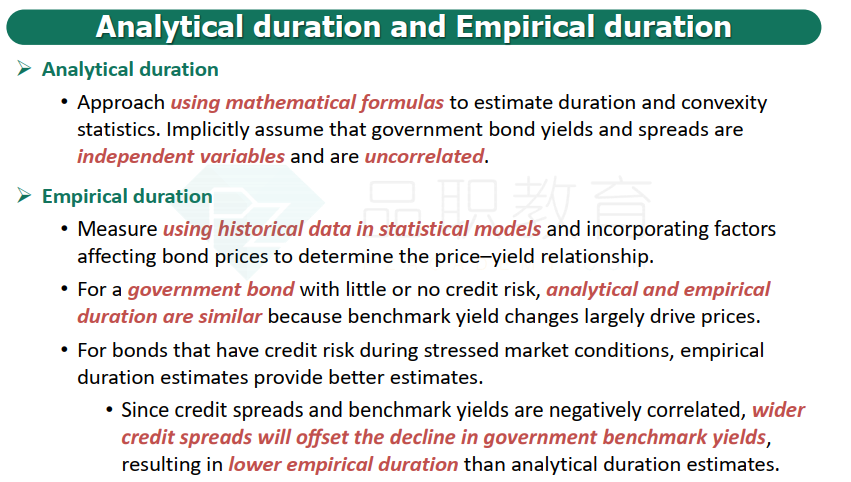

Empirical duration is likely the best measure of the impact of yield changes on portfolio value, especially under stressed market conditions, for a portfolio consisting of:

选项:

A.

100% sovereign bonds of several AAA rated euro area issuers.

B.

100% covered bonds of several AAA rated euro area corporate issuers.

C.

25% AAA rated sovereign bonds, 25% AAA rated corporate bonds, and 50% high-yield (i.e., speculative-grade) corporate bonds, all from various euro area sovereign and corporate issuers.

解释:

C is correct. Empirical duration is the best measure—better than analytical duration—of the impact of yield changes on portfolio value, especially under stressed market conditions, for a portfolio consisting of a variety of different bonds from different issuers, such as the portfolio described in Answer C. In this portfolio, credit spread changes on the high-yield bonds may partly or fully offset yield changes on the AAA rated sovereign bonds and spread changes on

the AAA rated corporate bonds; this interaction is best captured using empirical duration. The portfolios described in Answers A and B consist of the same types of bonds from similar issuers—sovereign bonds from similar-rated sovereign issuers (A) and covered bonds from similar-rated corporate issuers (B)—so empirical and analytical durations should be roughly similar in each of these portfolios.

考点:Empirical duration

解析:对于一个由不同发行人发行的各种不同债券组成的投资组合,empirical duration为更好的度量。高收益债券的信用利差变化可能部分或全部抵消AAA级主权债券收益率的变化和信用利差的变化,故选项C正确。

利差是什么?这个解释看了还是不知道啥意思